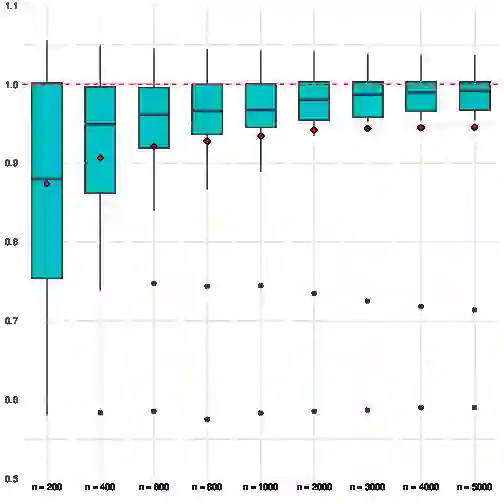

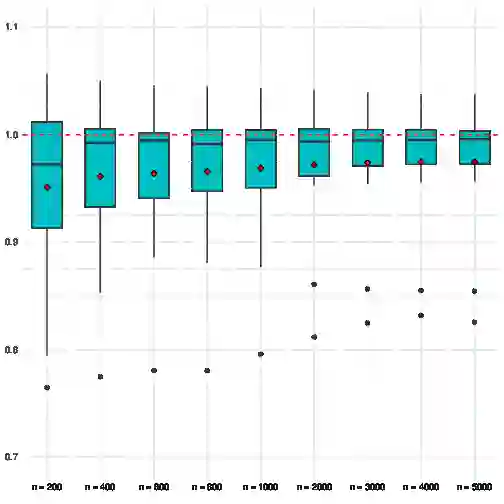

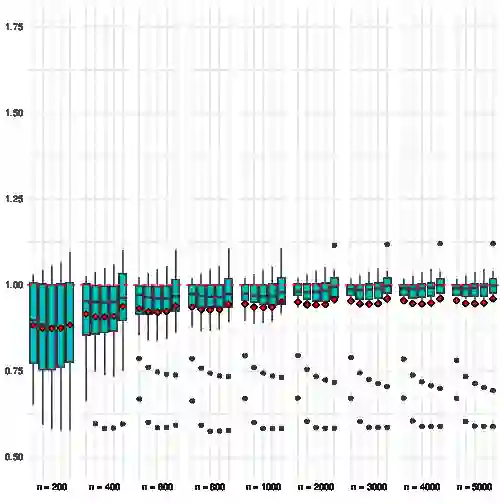

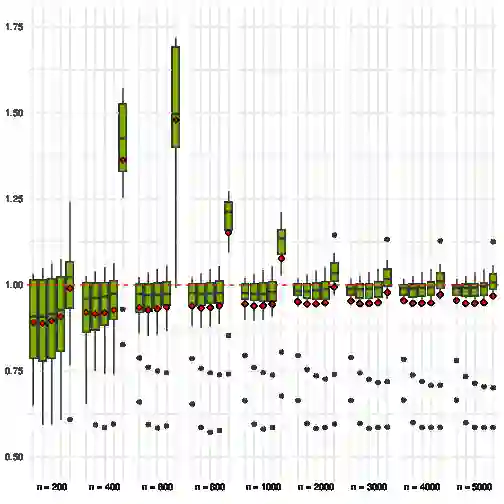

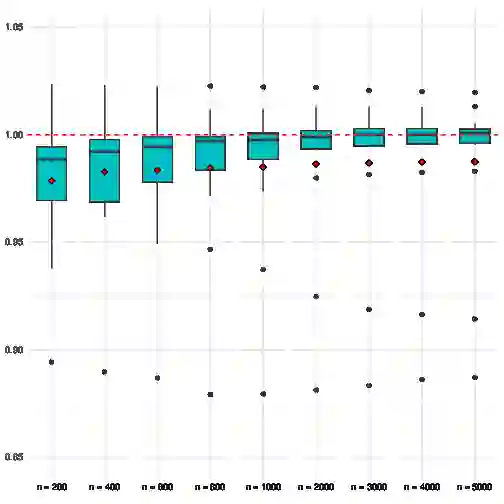

This papers proposes a generic, high-level methodology for generating forecast combinations that would deliver the optimal linearly combined forecast in terms of the mean-squared forecast error if one had access to two population quantities: the mean vector and the covariance matrix of the vector of individual forecast errors. We point out that this problem is identical to a mean-variance portfolio construction problem, in which portfolio weights correspond to forecast combination weights. We allow negative forecast weights and interpret such weights as hedging over and under estimation risks across estimators. This interpretation follows directly as an implication of the portfolio analogy. We demonstrate our method's improved out-of-sample performance relative to standard methods in combining tree forecasts to form weighted random forests in 14 data sets.

翻译:本文提出了一种通用的高阶方法论,用于生成预测组合,该方法在能够获取两个总体量(即各预测误差向量的均值向量与协方差矩阵)的条件下,可实现基于均方预测误差准则的最优线性组合预测。我们指出该问题与均值-方差投资组合构建问题具有同构性,其中投资组合权重对应预测组合权重。我们允许预测权重取负值,并将此类权重解释为对不同估计量间过高与过低估计风险的对冲操作。这一解释直接源于投资组合类比的理论推演。通过在14个数据集中对树预测进行组合以构建加权随机森林的实证分析,我们证明了该方法相较于标准方法在样本外表现方面具有显著改进。