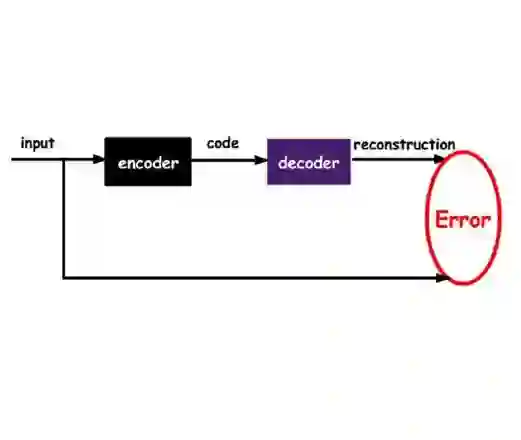

Stress testing refers to the application of adverse financial or macroeconomic scenarios to a portfolio. For this purpose, financial or macroeconomic risk factors are linked with asset returns, typically via a factor model. We expand the range of risk factors by adapting dimension-reduction techniques from unsupervised learning, namely PCA and autoencoders. This results in aggregated risk factors, encompassing a global factor, factors representing broad geographical regions, and factors specific to cyclical and defensive industries. As the adapted PCA and autoencoders provide an interpretation of the latent factors, this methodology is also valuable in other areas where dimension-reduction and explainability are crucial.

翻译:压力测试是指将不利的金融或宏观经济情景应用于投资组合。为此,金融或宏观经济风险因子通常通过因子模型与资产收益相关联。我们通过采用无监督学习中的降维技术(即主成分分析(PCA)和自编码器)来扩展风险因子的范围。由此生成聚合风险因子,涵盖全球因子、代表广泛地理区域的因子,以及针对周期性行业和防御性行业的特定因子。由于改进后的PCA和自编码器能够提供潜在因子的解释,这一方法论在需要降维和可解释性的其他领域同样具有重要价值。