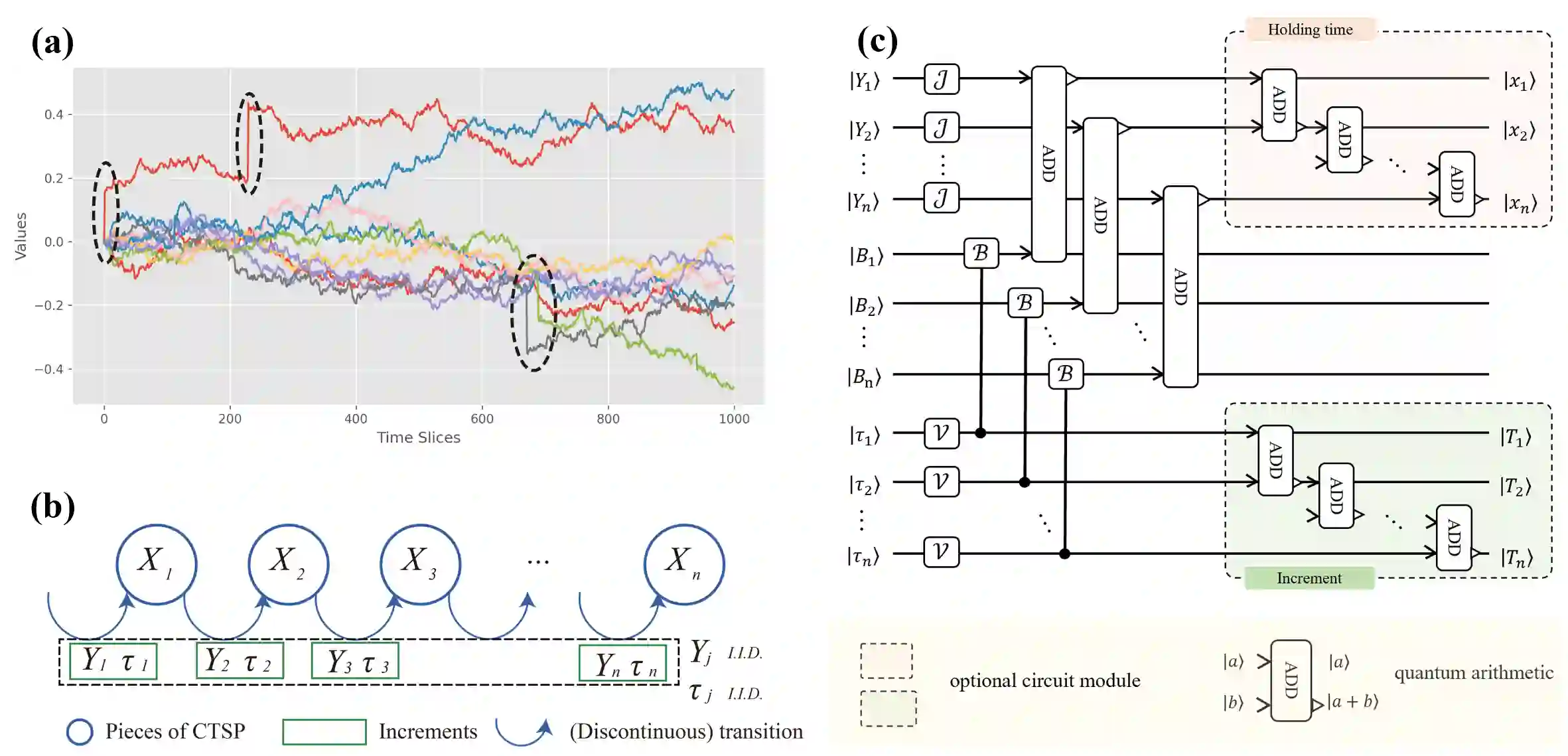

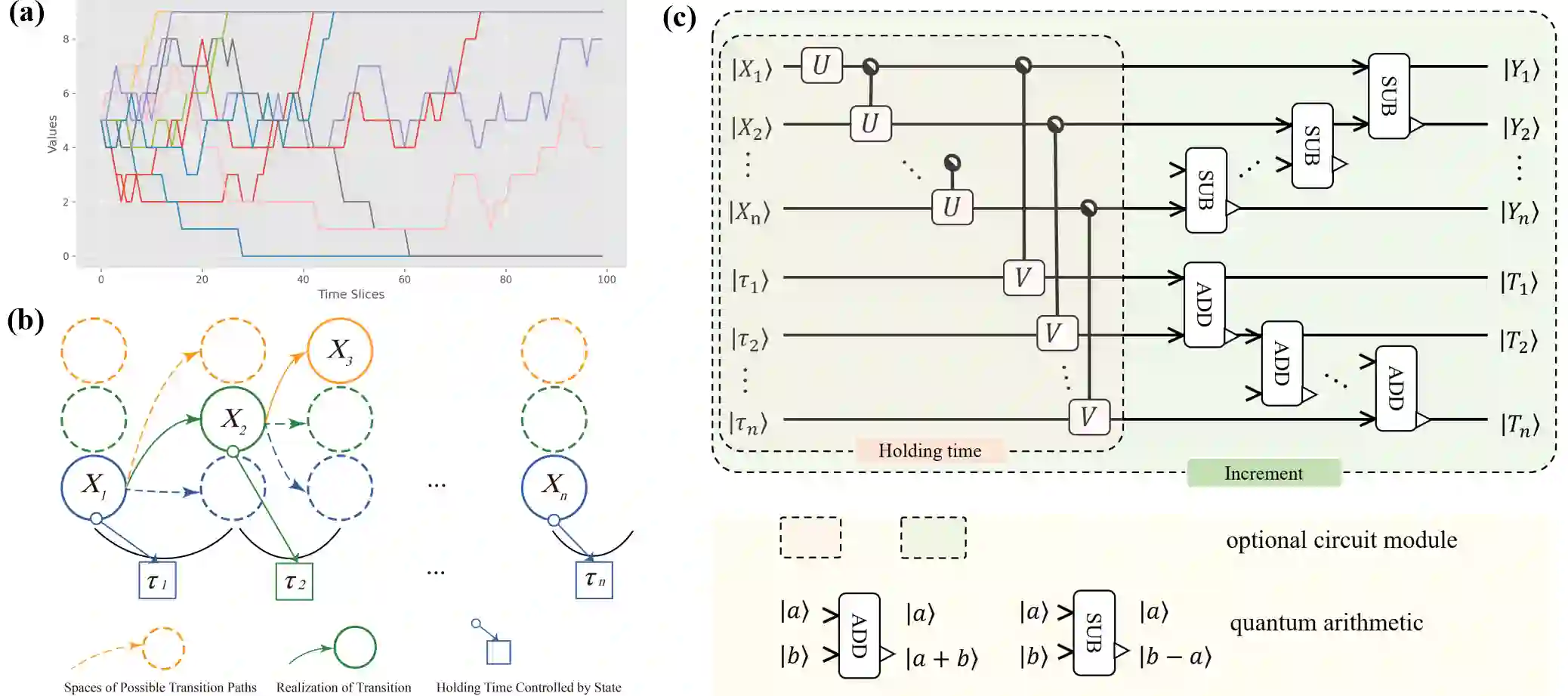

The continuous time stochastic process is a mainstream mathematical instrument modeling the random world with a wide range of applications involving finance, statistics, physics, and time series analysis, while the simulation and analysis of the continuous time stochastic process is a challenging problem for classical computers. In this work, a general framework is established to prepare the path of a continuous time stochastic process in a quantum computer efficiently. The storage and computation resource is exponentially reduced on the key parameter of holding time, as the qubit number and the circuit depth are both optimized via our compressed state preparation method. The desired information, including the path-dependent and history-sensitive information that is essential for financial problems, can be extracted efficiently from the compressed sampling path, and admits a further quadratic speed-up. Moreover, this extraction method is more sensitive to those discontinuous jumps capturing extreme market events. Two applications of option pricing in Merton jump diffusion model and ruin probability computing in the collective risk model are given.

翻译:连续时间随机过程是描述随机世界的主流数学工具,广泛应用于金融、统计、物理和时间序列分析等领域,然而在经典计算机上对连续时间随机过程进行模拟与分析仍是一项具有挑战性的问题。本文建立了一个通用框架,可在量子计算机上高效制备连续时间随机过程的路径。通过我们提出的压缩态制备方法,储存与计算资源在关键参数——持仓时间上呈指数级缩减,量子比特数与电路深度均得到优化。对于金融问题至关重要的路径依赖型与历史敏感型信息,可以从压缩采样路径中高效提取,并实现二次加速。此外,该提取方法对捕捉极端市场事件的非连续跳跃更为敏感。本文给出了默顿跳扩散模型中的期权定价与集体风险模型中的破产概率计算两个应用实例。

相关内容

Source: Apple - iOS 8