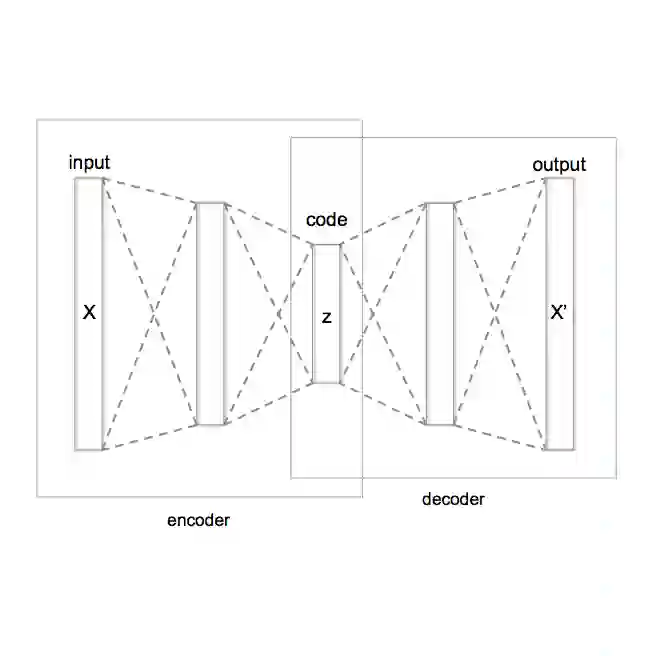

In this research, we propose a novel approach for the quantification of credit portfolio Value-at-Risk (VaR) sensitivity to asset correlations with the use of synthetic financial correlation matrices generated with deep learning models. In previous work Generative Adversarial Networks (GANs) were employed to demonstrate the generation of plausible correlation matrices, that capture the essential characteristics observed in empirical correlation matrices estimated on asset returns. Instead of GANs, we employ Variational Autoencoders (VAE) to achieve a more interpretable latent space representation. Through our analysis, we reveal that the VAE latent space can be a useful tool to capture the crucial factors impacting portfolio diversification, particularly in relation to credit portfolio sensitivity to asset correlations changes.

翻译:本研究提出了一种新方法,利用深度学习模型生成的合成金融相关性矩阵,量化信用组合在险价值(VaR)对资产相关性的敏感性。此前的研究采用生成对抗网络(GAN)生成具有合理性的相关性矩阵,这些矩阵能够捕捉基于资产收益率估计的实证相关性矩阵的关键特征。本研究摒弃GAN,转而采用变分自编码器(VAE)以实现更具可解释性的隐空间表征。通过分析发现,VAE隐空间可作为有效工具捕获影响组合多样化的关键因素,特别是在信用组合对资产相关性变化的敏感性分析中。