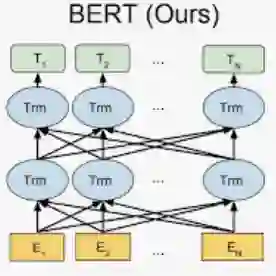

With the rapid development of big data and computing devices, low-latency automatic trading platforms based on real-time information acquisition have become the main components of the stock trading market, so the topic of quantitative trading has received widespread attention. And for non-strongly efficient trading markets, human emotions and expectations always dominate market trends and trading decisions. Therefore, this paper starts from the theory of emotion, taking East Money as an example, crawling user comment titles data from its corresponding stock bar and performing data cleaning. Subsequently, a natural language processing model BERT was constructed, and the BERT model was fine-tuned using existing annotated data sets. The experimental results show that the fine-tuned model has different degrees of performance improvement compared to the original model and the baseline model. Subsequently, based on the above model, the user comment data crawled is labeled with emotional polarity, and the obtained label information is combined with the Alpha191 model to participate in regression, and significant regression results are obtained. Subsequently, the regression model is used to predict the average price change for the next five days, and use it as a signal to guide automatic trading. The experimental results show that the incorporation of emotional factors increased the return rate by 73.8\% compared to the baseline during the trading period, and by 32.41\% compared to the original alpha191 model. Finally, we discuss the advantages and disadvantages of incorporating emotional factors into quantitative trading, and give possible directions for further research in the future.

翻译:随着大数据与计算设备的快速发展,基于实时信息采集的低延迟自动交易平台已成为股票交易市场的主要组成部分,量化交易课题因此受到广泛关注。对于非强有效交易市场而言,人类情绪与预期始终主导市场趋势及交易决策。因此,本文从情感理论出发,以东方财富为例,爬取其对应股票吧中的用户评论标题数据并进行数据清洗。随后构建自然语言处理模型BERT,并利用已有标注数据集对BERT模型进行微调。实验结果表明,相较于原始模型与基线模型,微调模型在性能上均有不同程度的提升。在此基础上,基于上述模型对爬取的用户评论数据进行情感极性标注,将获得的标签信息结合Alpha191模型参与回归,并取得了显著的回归结果。随后,利用回归模型预测未来五日的平均价格变化,并将其作为信号指导自动交易。实验结果显示,在交易期间,融入情感因子相较于基线模型收益率提升73.8%,相较于原始Alpha191模型提升32.41%。最后,本文探讨了将情感因子引入量化交易的优缺点,并给出了未来进一步研究的可能方向。