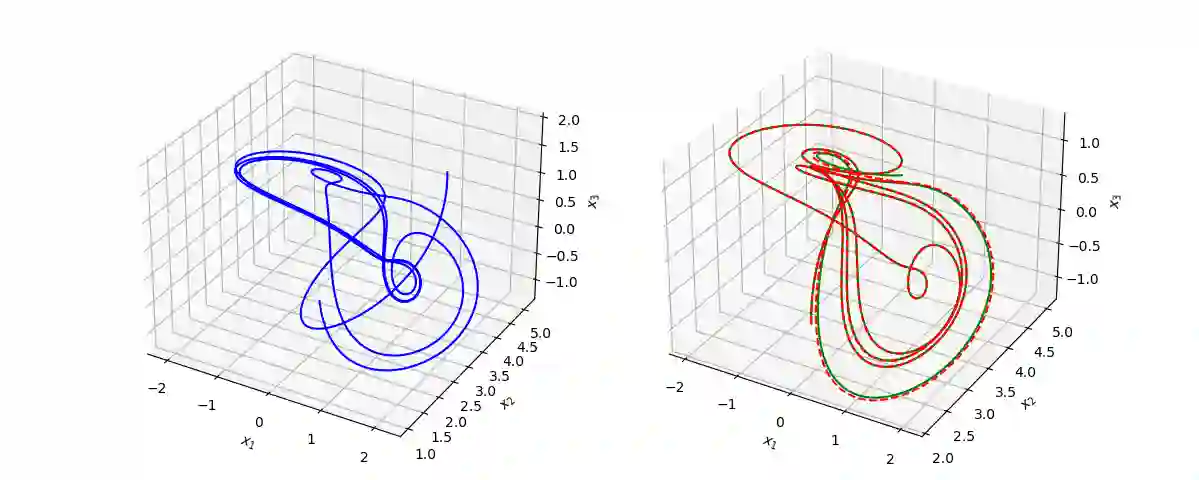

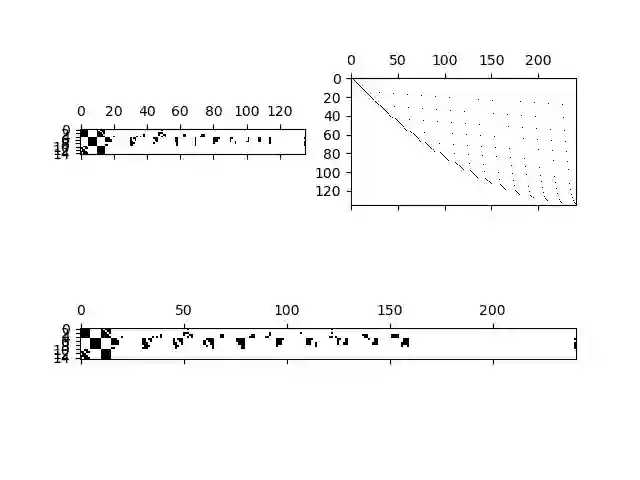

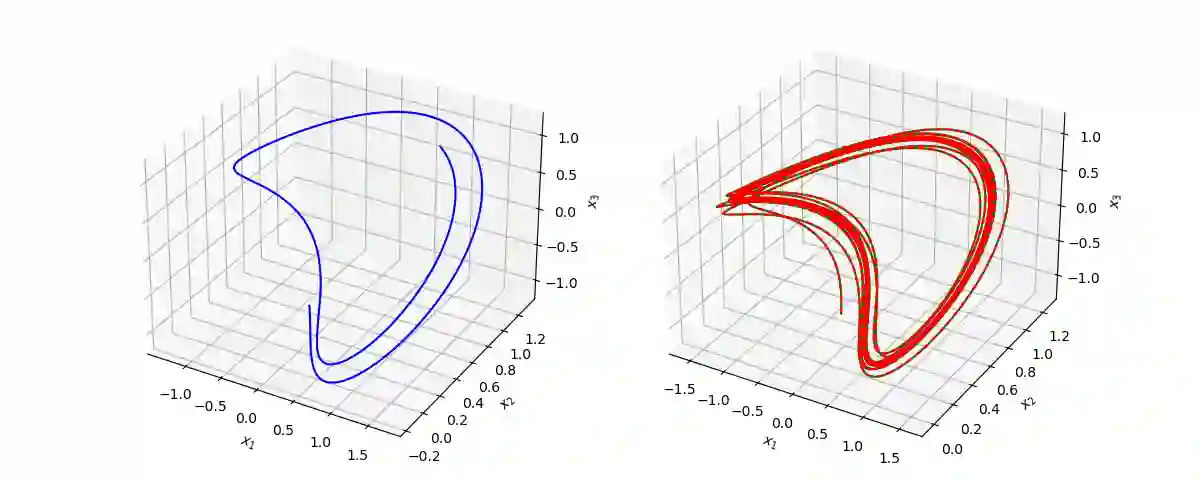

In this document, we present key findings in structured matrix approximation theory, with applications to the regressive representation of dynamic financial processes. Initially, we explore a comprehensive approach involving generic nonlinear time delay embedding for time series data extracted from a financial or economic system under examination. Subsequently, we employ sparse least-squares and structured matrix approximation methods to discern approximate representations of the output coupling matrices. These representations play a pivotal role in establishing the regressive models corresponding to the recursive structures inherent in a given financial system. The document further introduces prototypical algorithms that leverage the aforementioned techniques. These algorithms are demonstrated through applications in approximate identification and predictive simulation of dynamic financial and economic processes, encompassing scenarios that may or may not exhibit chaotic behavior.

翻译:本文介绍了结构矩阵逼近理论的关键发现及其在动态金融过程回归表示中的应用。首先,我们探索了一种综合方法,涉及对所研究的金融或经济系统提取的时间序列数据进行通用非线性时延嵌入。随后,我们采用稀疏最小二乘法和结构矩阵逼近方法,来辨识输出耦合矩阵的近似表示。这些表示在建立与给定金融系统内在递归结构相对应的回归模型中起着关键作用。本文进一步介绍了利用上述技术的原型算法。这些算法通过应用于动态金融和经济过程的近似辨识与预测模拟(包括可能呈现混沌行为的情景)进行了展示。