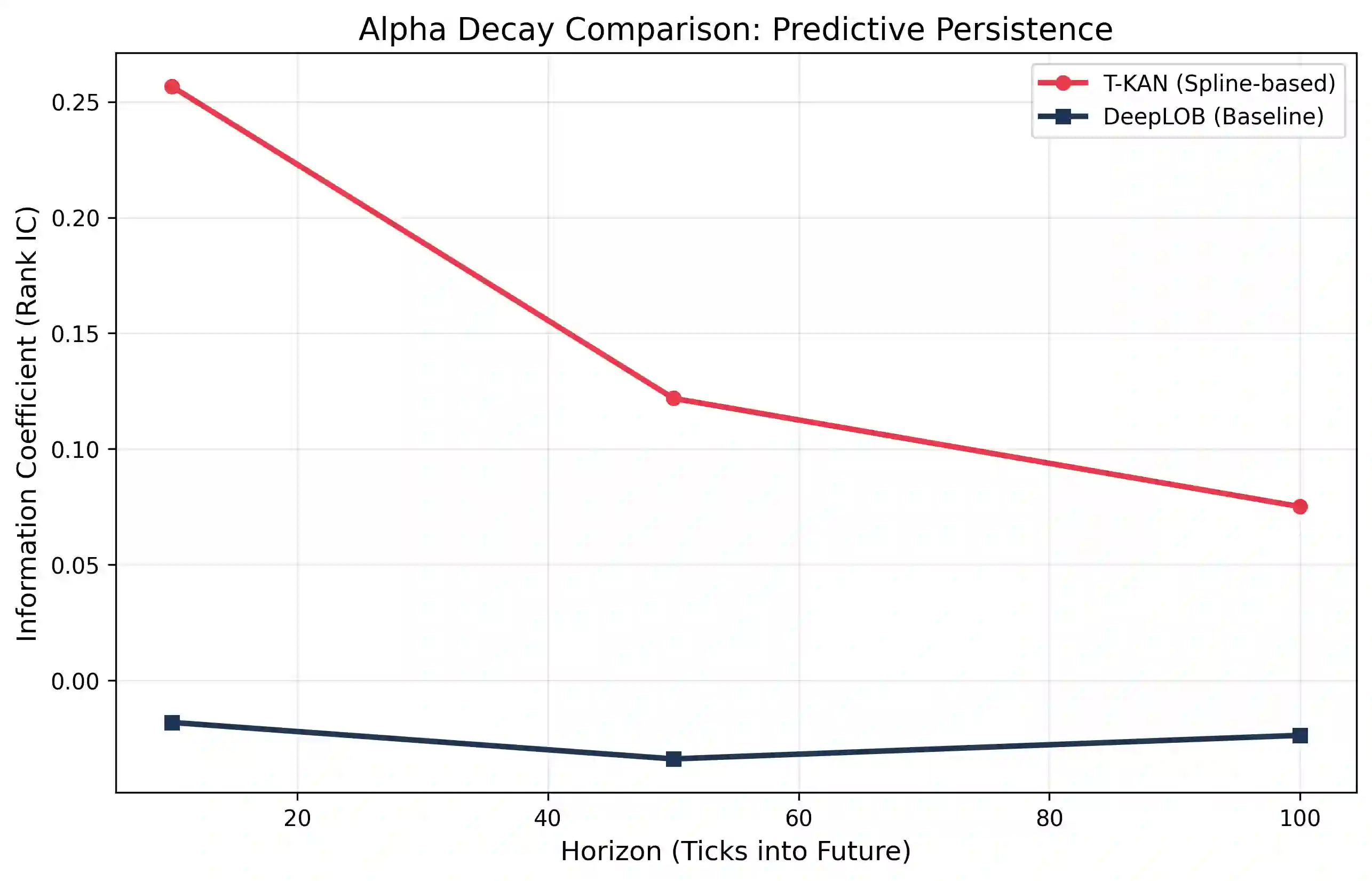

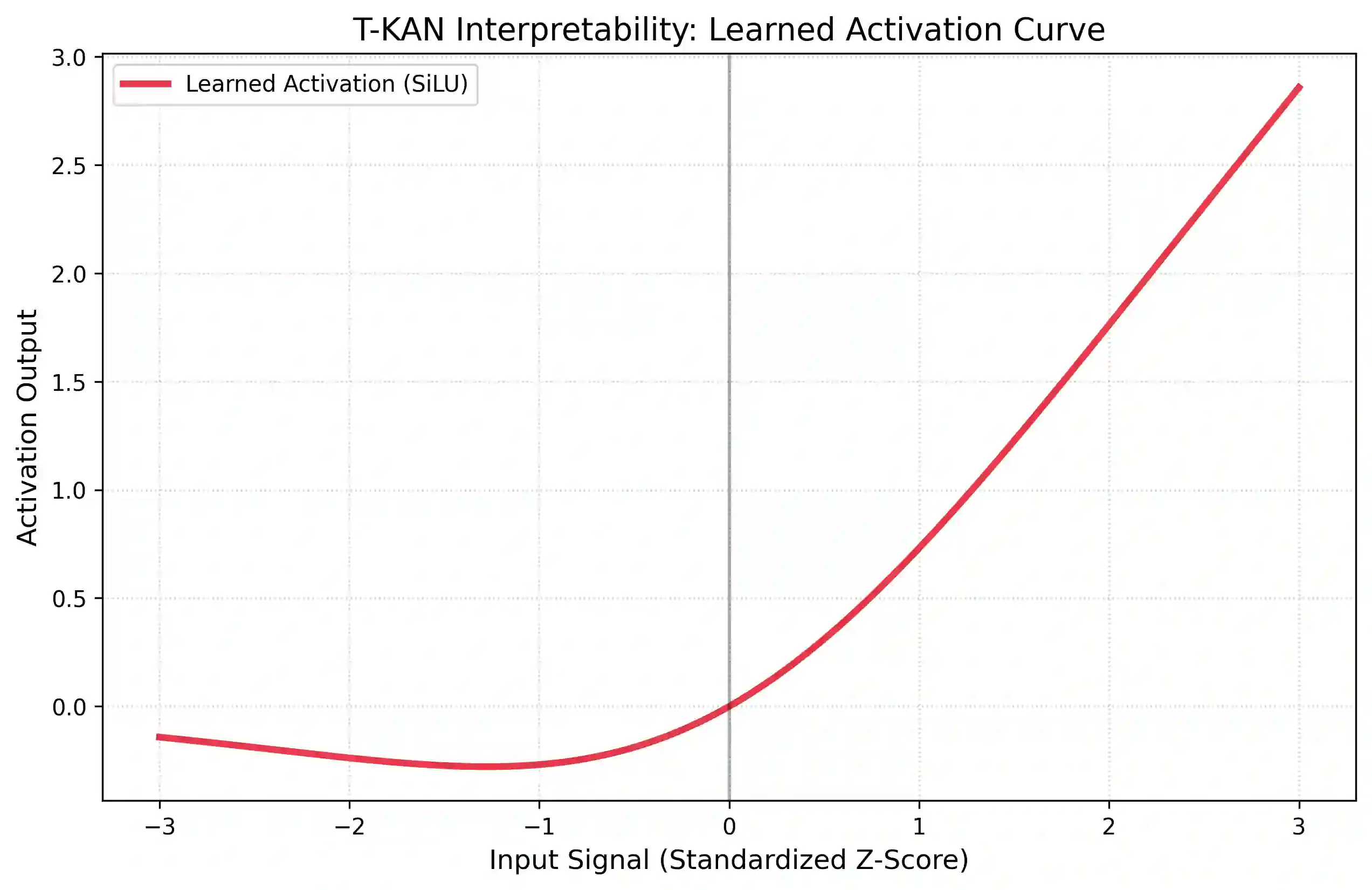

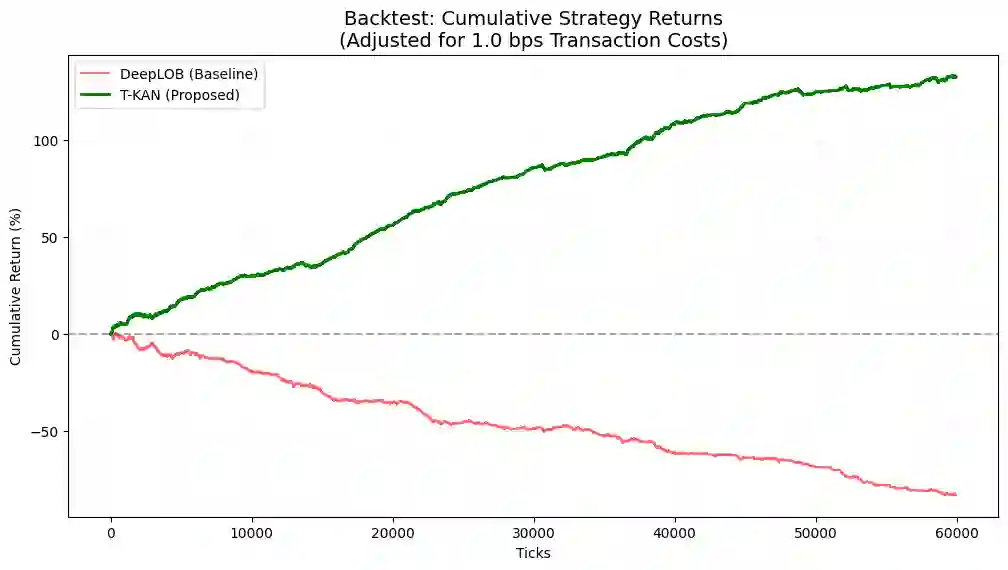

High-Frequency trading (HFT) environments are characterised by large volumes of limit order book (LOB) data, which is notoriously noisy and non-linear. Alpha decay represents a significant challenge, with traditional models such as DeepLOB losing predictive power as the time horizon (k) increases. In this paper, using data from the FI-2010 dataset, we introduce Temporal Kolmogorov-Arnold Networks (T-KAN) to replace the fixed, linear weights of standard LSTMs with learnable B-spline activation functions. This allows the model to learn the 'shape' of market signals as opposed to just their magnitude. This resulted in a 19.1% relative improvement in the F1-score at the k = 100 horizon. The efficacy of T-KAN networks cannot be understated, producing a 132.48% return compared to the -82.76% DeepLOB drawdown under 1.0 bps transaction costs. In addition to this, the T-KAN model proves quite interpretable, with the 'dead-zones' being clearly visible in the splines. The T-KAN architecture is also uniquely optimized for low-latency FPGA implementation via High level Synthesis (HLS). The code for the experiments in this project can be found at https://github.com/AhmadMak/Temporal-Kolmogorov-Arnold-Networks-T-KAN-for-High-Frequency-Limit-Order-Book-Forecasting.

翻译:高频交易环境以海量限价订单簿数据为特征,这些数据通常具有显著的噪声和非线性特性。Alpha衰减构成了重大挑战,传统模型(如DeepLOB)随着时间窗口的扩展会逐渐丧失预测能力。本文基于FI-2010数据集,提出时序Kolmogorov-Arnold网络,通过可学习的B样条激活函数替代标准LSTM中固定的线性权重。这使得模型能够学习市场信号的“形态特征”而不仅是幅度信息。该方法在k=100时间窗口的F1分数上实现了19.1%的相对提升。T-KAN网络的有效性尤为突出,在1.0个基点的交易成本下获得132.48%的收益率,而DeepLOB策略则出现-82.76%的最大回撤。此外,T-KAN模型展现出良好的可解释性,其样条函数中可清晰辨识“无效区间”。该架构还通过高层次综合技术针对低延迟FPGA实现进行了专门优化。本实验代码详见:https://github.com/AhmadMak/Temporal-Kolmogorov-Arnold-Networks-T-KAN-for-High-Frequency-Limit-Order-Book-Forecasting。