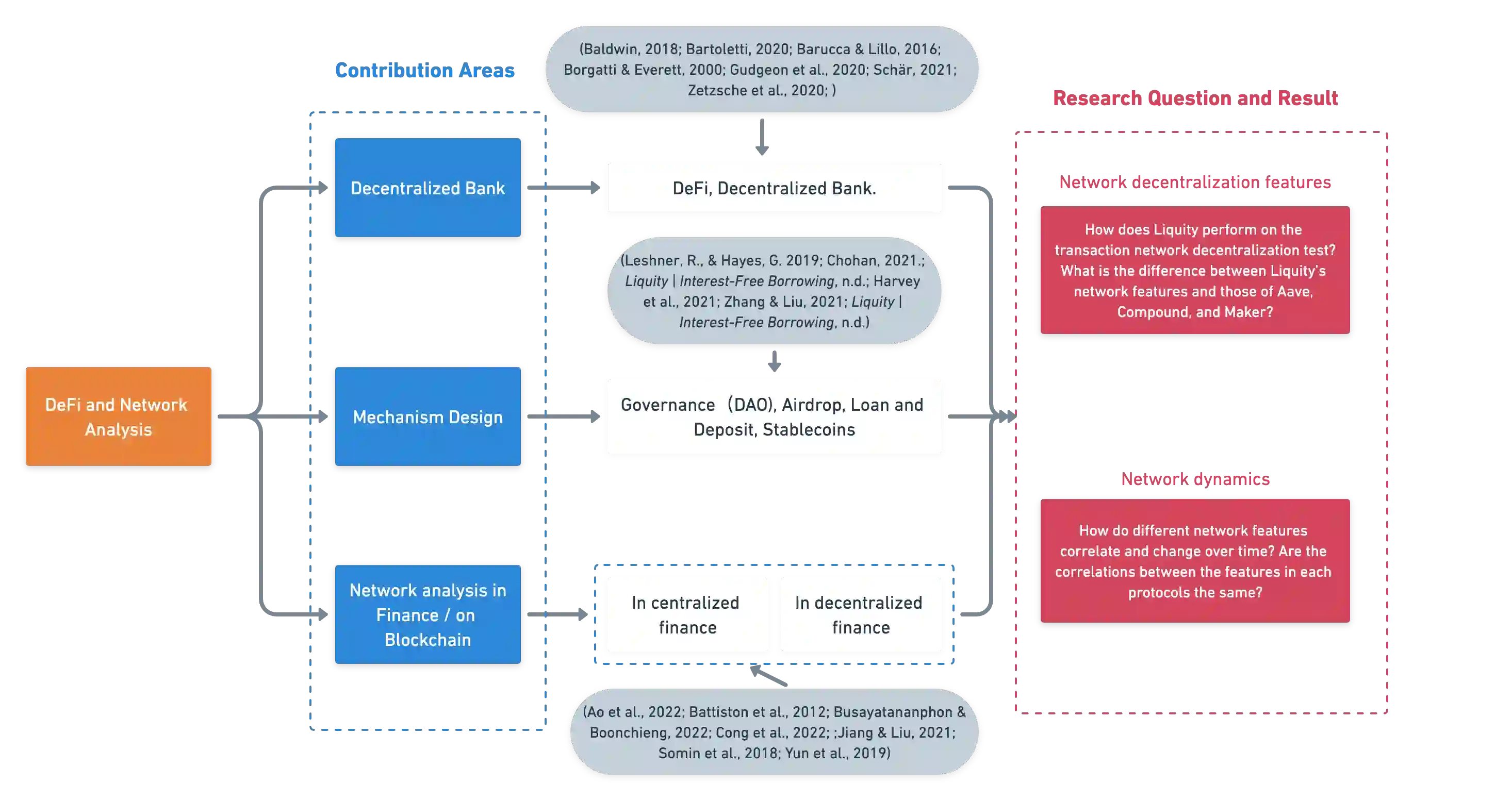

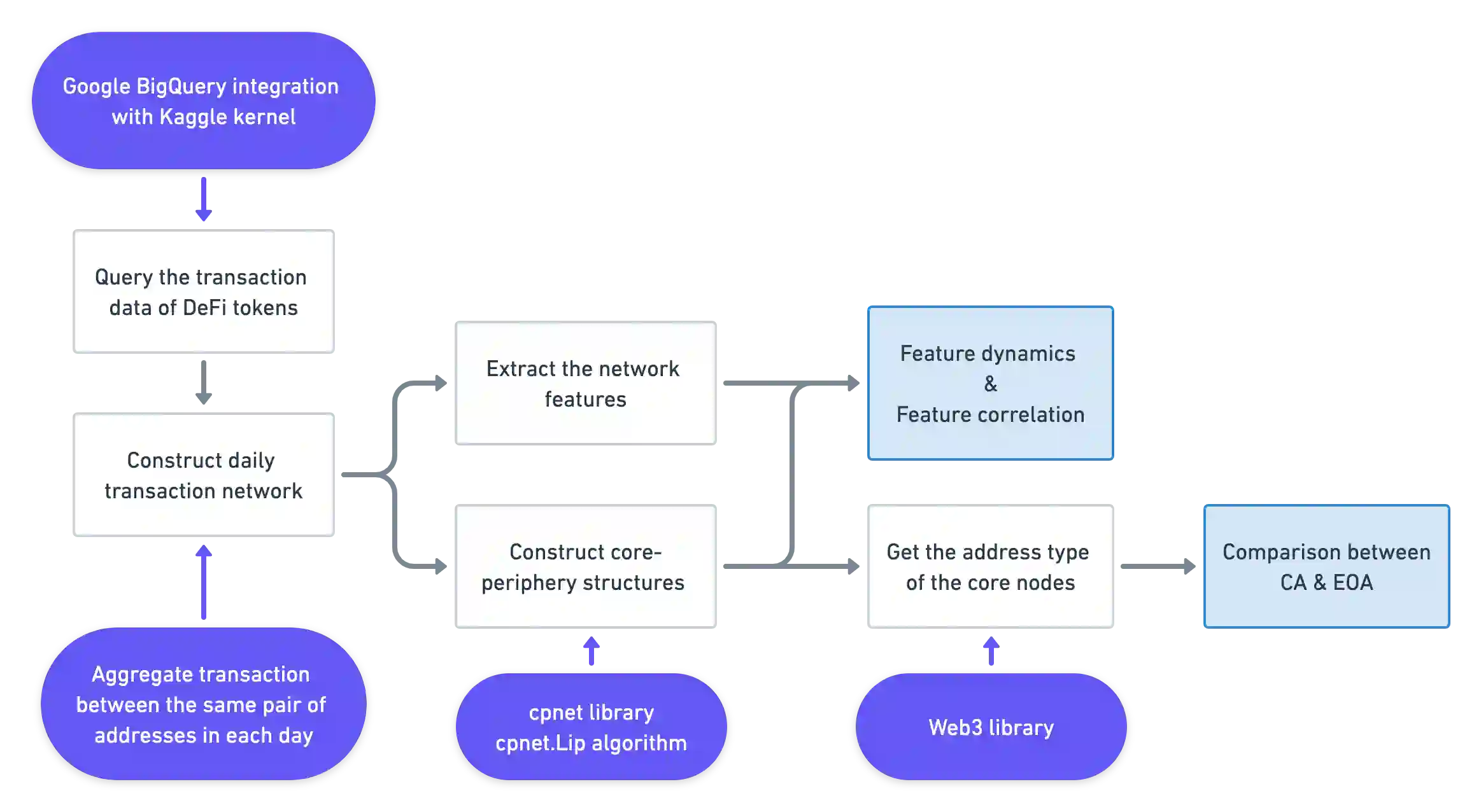

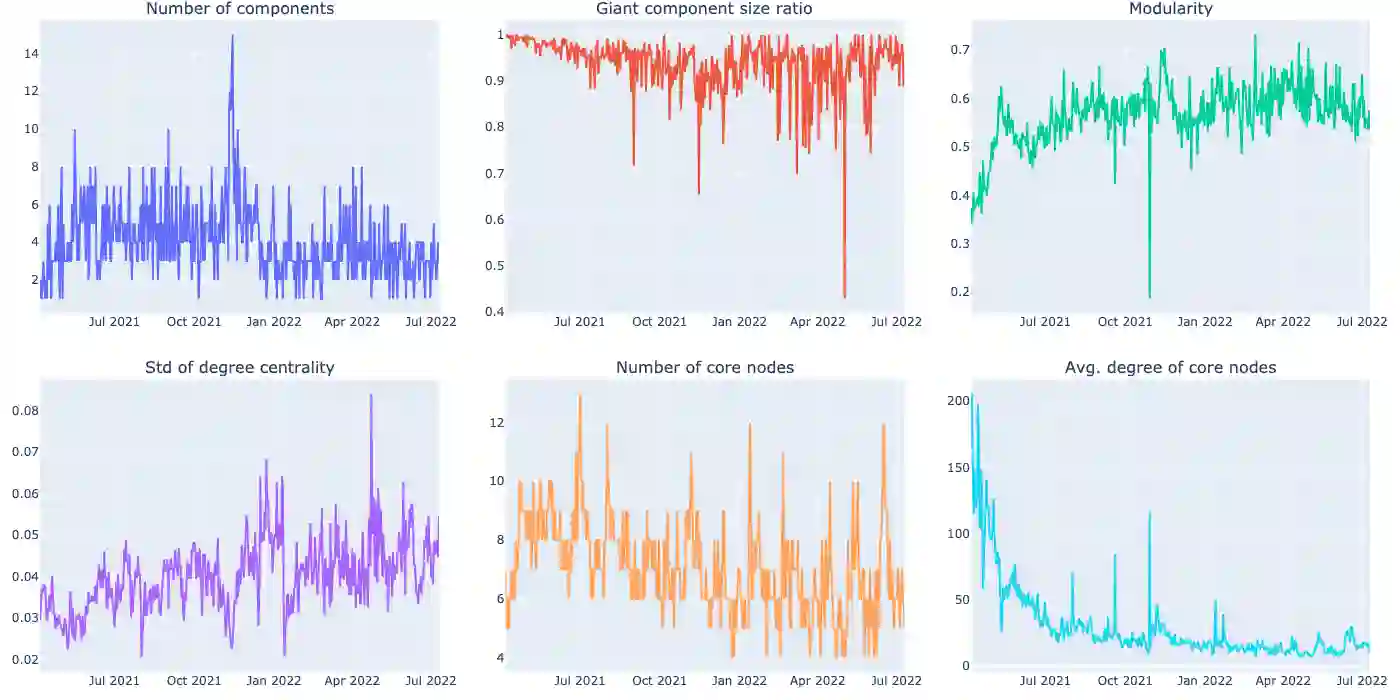

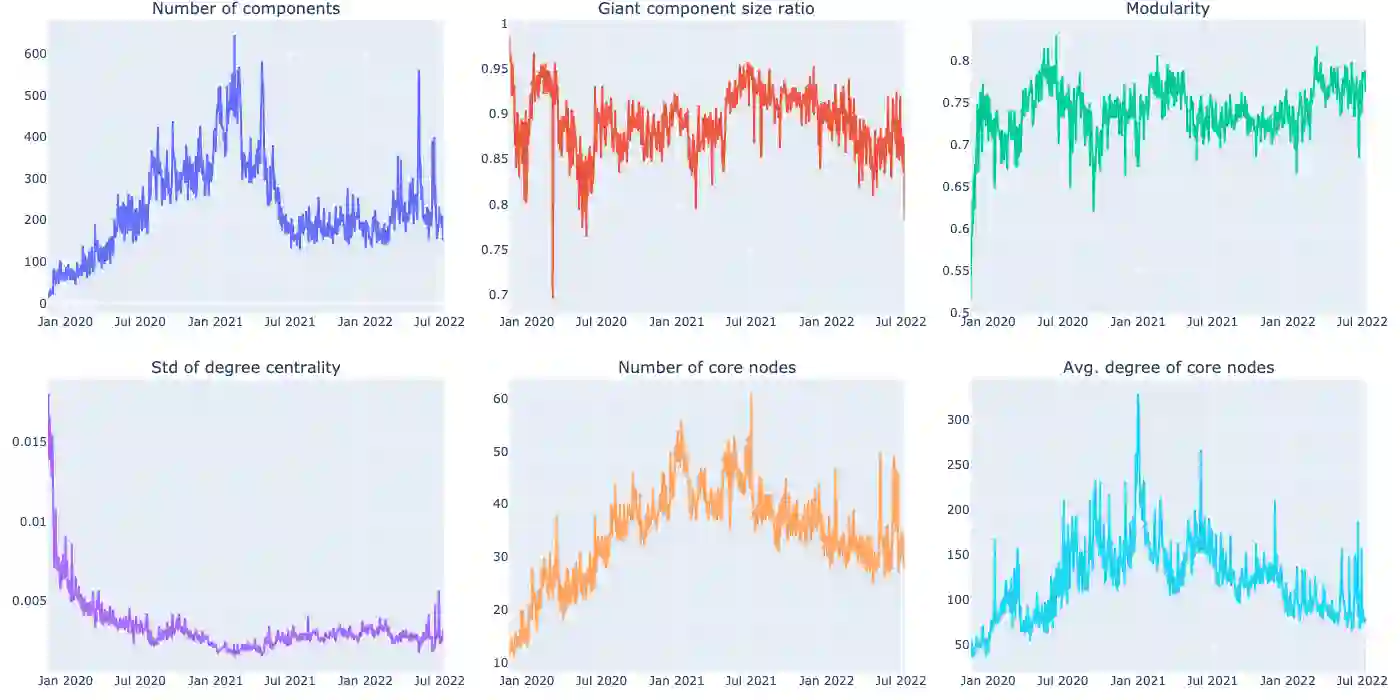

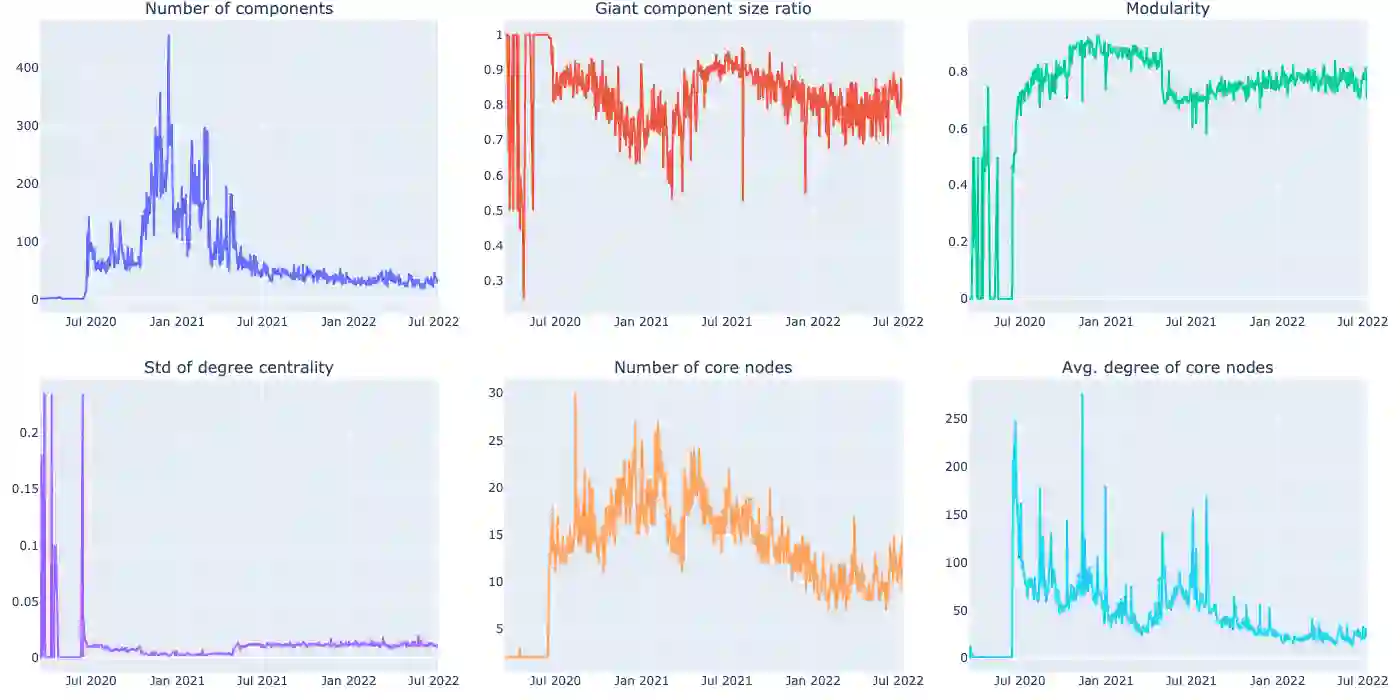

Decentralized finance (DeFi) is known for its unique mechanism design, which applies smart contracts to facilitate peer-to-peer transactions. The decentralized bank is a typical DeFi application. Ideally, a decentralized bank should be decentralized in the transaction. However, many recent studies have found that decentralized banks have not achieved a significant degree of decentralization. This research conducts a comparative study among mainstream decentralized banks. We apply core-periphery network features analysis using the transaction data from four decentralized banks, Liquity, Aave, MakerDao, and Compound. We extract six features and compare the banks' levels of decentralization cross-sectionally. According to the analysis results, we find that: 1) MakerDao and Compound are more decentralized in the transactions than Aave and Liquity. 2) Although decentralized banking transactions are supposed to be decentralized, the data show that four banks have primary external transaction core addresses such as Huobi, Coinbase, and Binance, etc. We also discuss four design features that might affect network decentralization. Our research contributes to the literature at the interface of decentralized finance, financial technology (Fintech), and social network analysis and inspires future protocol designs to live up to the promise of decentralized finance for a truly peer-to-peer transaction network.

翻译:去中心化金融(DeFi)以其独特的机制设计而闻名,通过应用智能合约促进点对点交易。去中心化银行是典型的DeFi应用。理想情况下,去中心化银行应在交易中实现去中心化。然而,近期多项研究发现,去中心化银行并未达到显著的的去中心化程度。本研究对主流去中心化银行进行了比较分析。我们利用Liquity、Aave、MakerDao和Compound四家去中心化银行的交易数据,采用核心-边缘网络特征分析方法,提取六项特征并横向比较各银行的去中心化水平。分析结果表明:1)MakerDao和Compound在交易中去中心化程度高于Aave和Liquity;2)尽管去中心化银行交易理应呈现去中心化特征,但数据显示四家银行均存在主要外部交易核心地址,例如Huobi、Coinbase和Binance等。我们还讨论了可能影响网络去中心化的四项设计特征。本研究为去中心化金融、金融科技(Fintech)与社会网络分析交叉领域的文献做出贡献,并启迪未来协议设计切实履行去中心化金融对真正点对点交易网络的承诺。