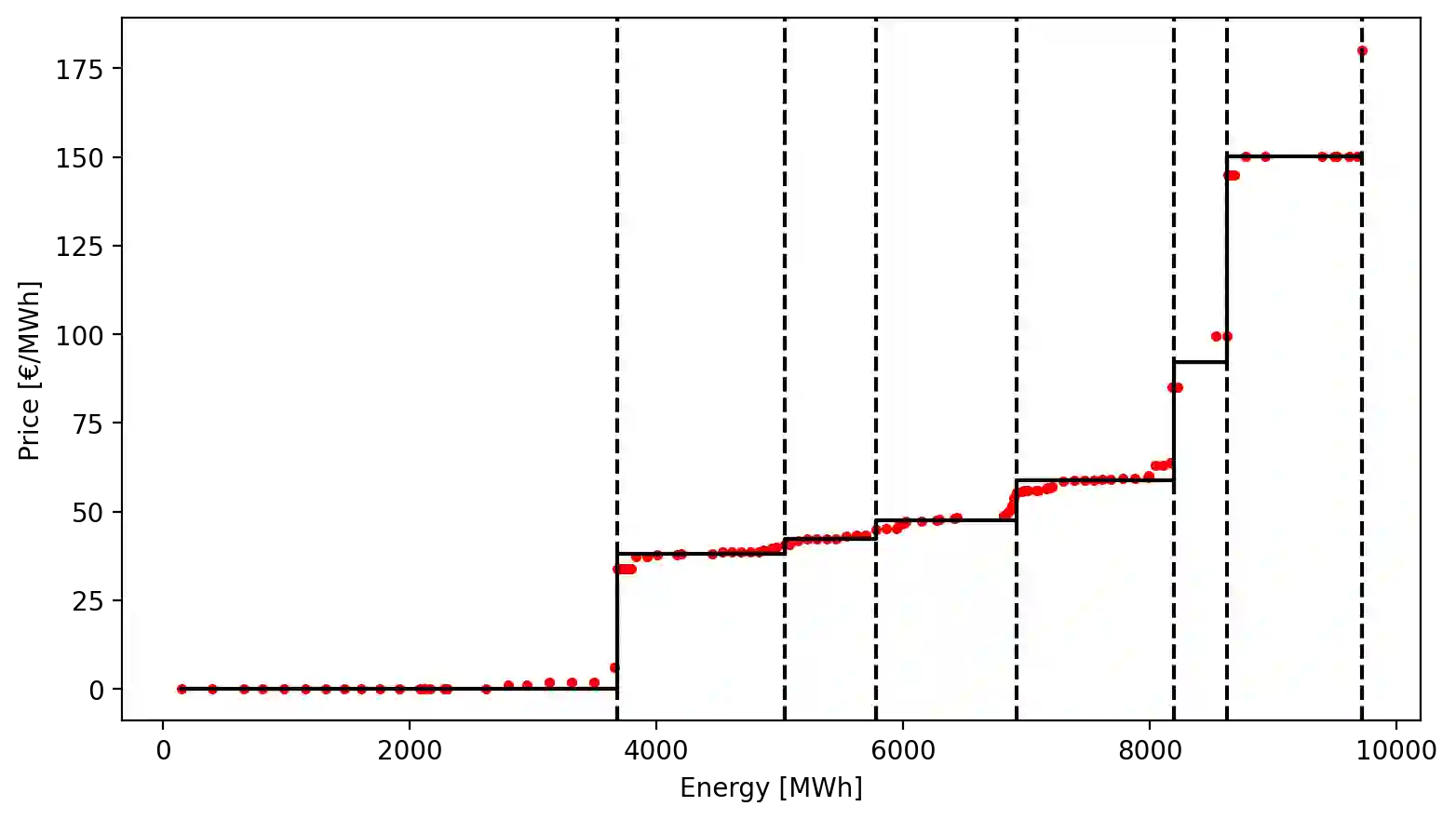

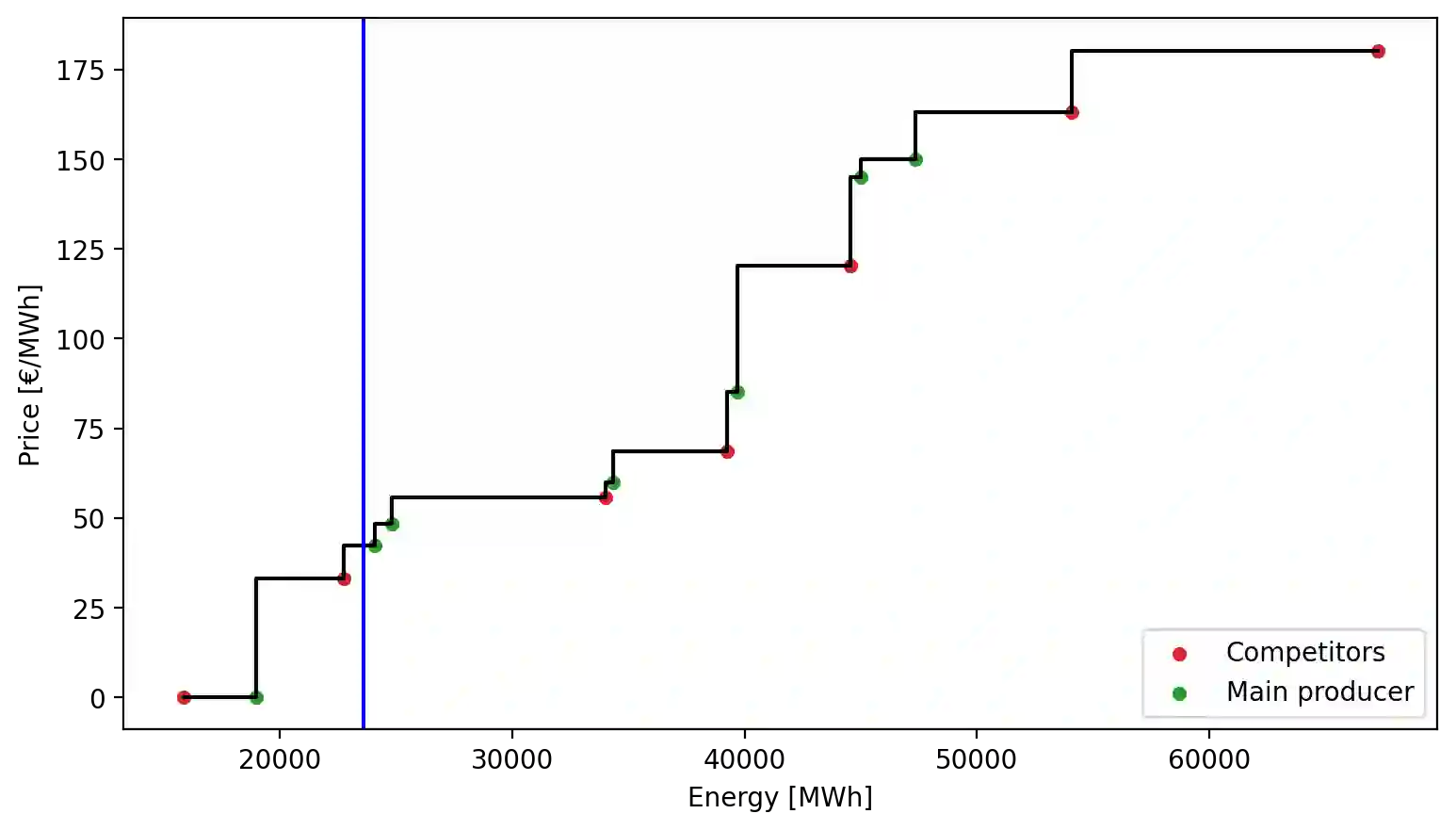

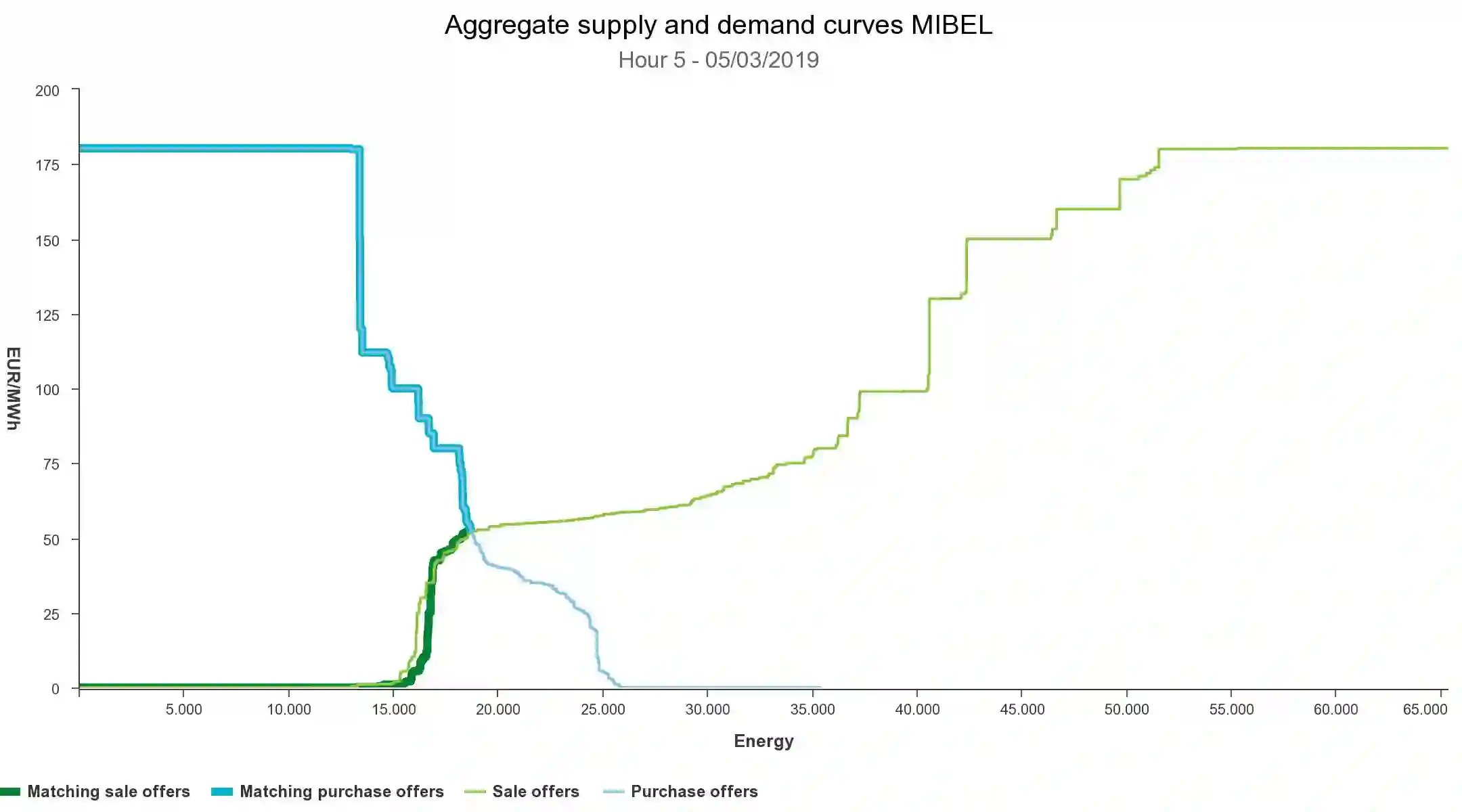

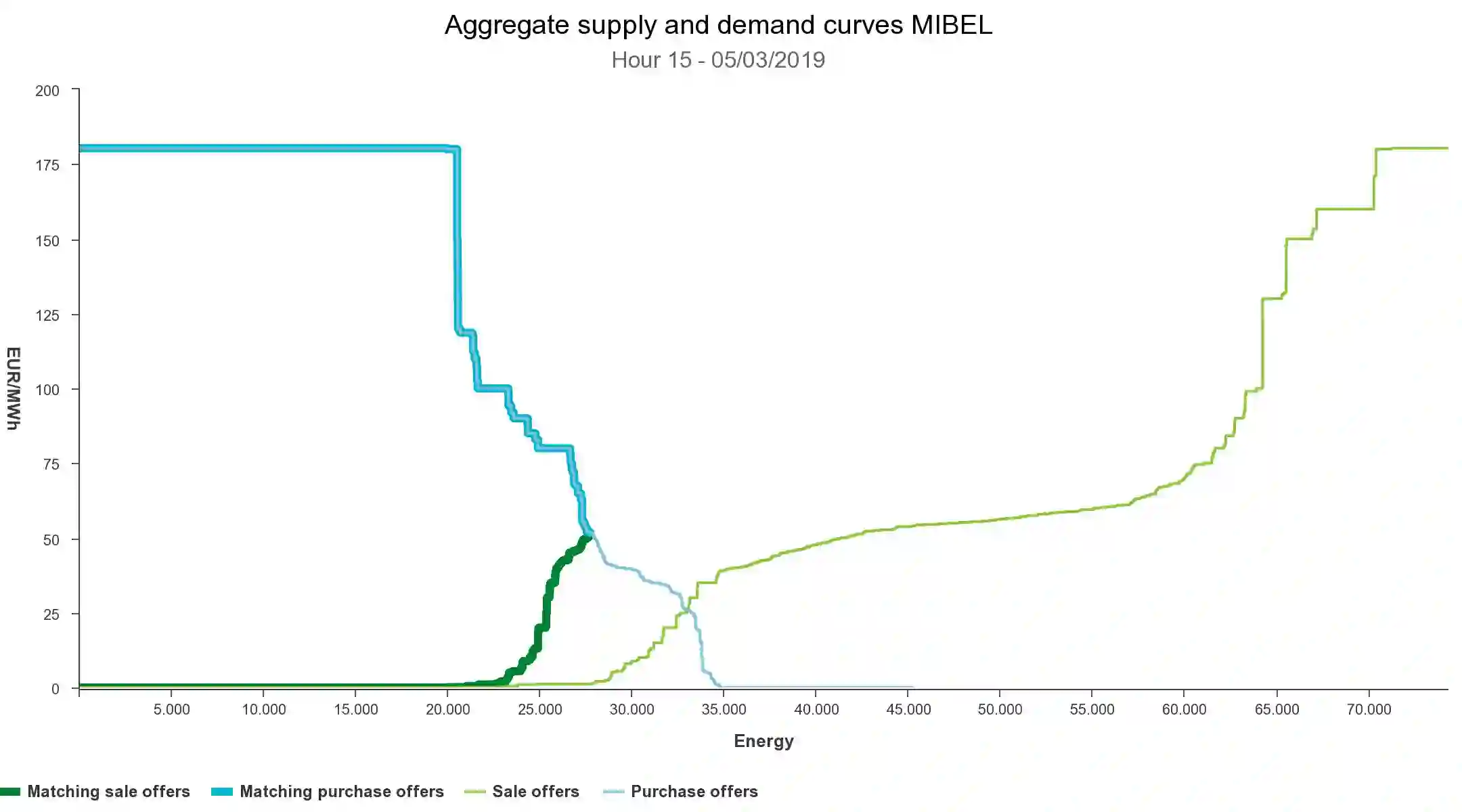

In day-ahead electricity markets based on uniform marginal pricing, small variations in the offering and bidding curves may substantially modify the resulting market outcomes. In this work, we deal with the problem of finding the optimal offering curve for a risk-averse profit-maximizing generating company (GENCO) in a data-driven context. In particular, a large GENCO's market share may imply that her offering strategy can alter the marginal price formation, which can be used to increase profit. We tackle this problem from a novel perspective. First, we propose a optimization-based methodology to summarize each GENCO's step-wise supply curves into a subset of representative price-energy blocks. Then, the relationship between the market price and the resulting energy block offering prices is modeled through a Bayesian linear regression approach, which also allows us to generate stochastic scenarios for the sensibility of the market towards the GENCO strategy, represented by the regression coefficient probabilistic distributions. Finally, this predictive model is embedded in the stochastic optimization model by employing a constraint learning approach. Results show how allowing the GENCO to deviate from her true marginal costs renders significant changes in her profits and the market marginal price. Furthermore, these results have also been tested in an out-of-sample validation setting, showing how this optimal offering strategy is also effective in a real-world market contest.

翻译:在基于统一边际定价的日前电力市场中,报价曲线的微小变化可能导致市场结果发生显著改变。本文从数据驱动视角出发,研究风险规避型利润最大化发电公司(GENCO)的最优报价曲线问题。特别地,大型GENCO的市场份额意味着其报价策略可能改变边际价格形成机制,从而为增加利润提供可能。我们采用创新方法解决该问题:首先,提出基于优化的方法论,将每个GENCO的阶梯式供应曲线归纳为若干代表性价格-能量区块;其次,通过贝叶斯线性回归方法建立市场价格与所得能量区块报价价格之间的关联模型,该模型还能基于回归系数概率分布生成市场对GENCO策略敏感度的随机场景;最后,采用约束学习方法将此预测模型嵌入随机优化模型。结果表明,允许GENCO偏离其真实边际成本将显著改变其利润与市场边际价格。同时,相关结果通过样本外验证测试,证明该最优报价策略在实际市场环境中同样有效。