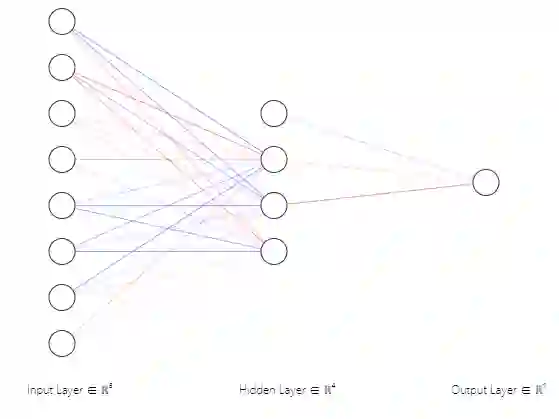

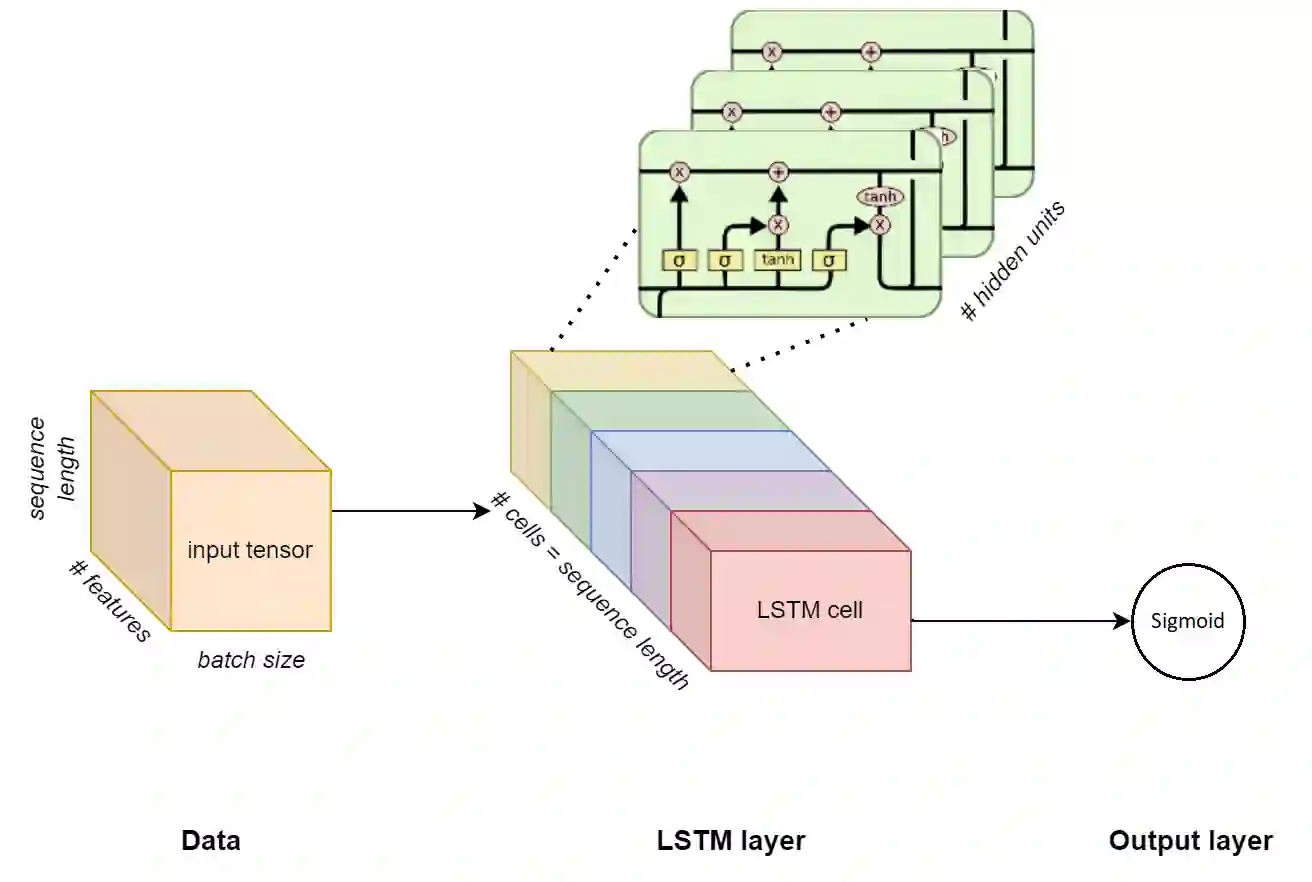

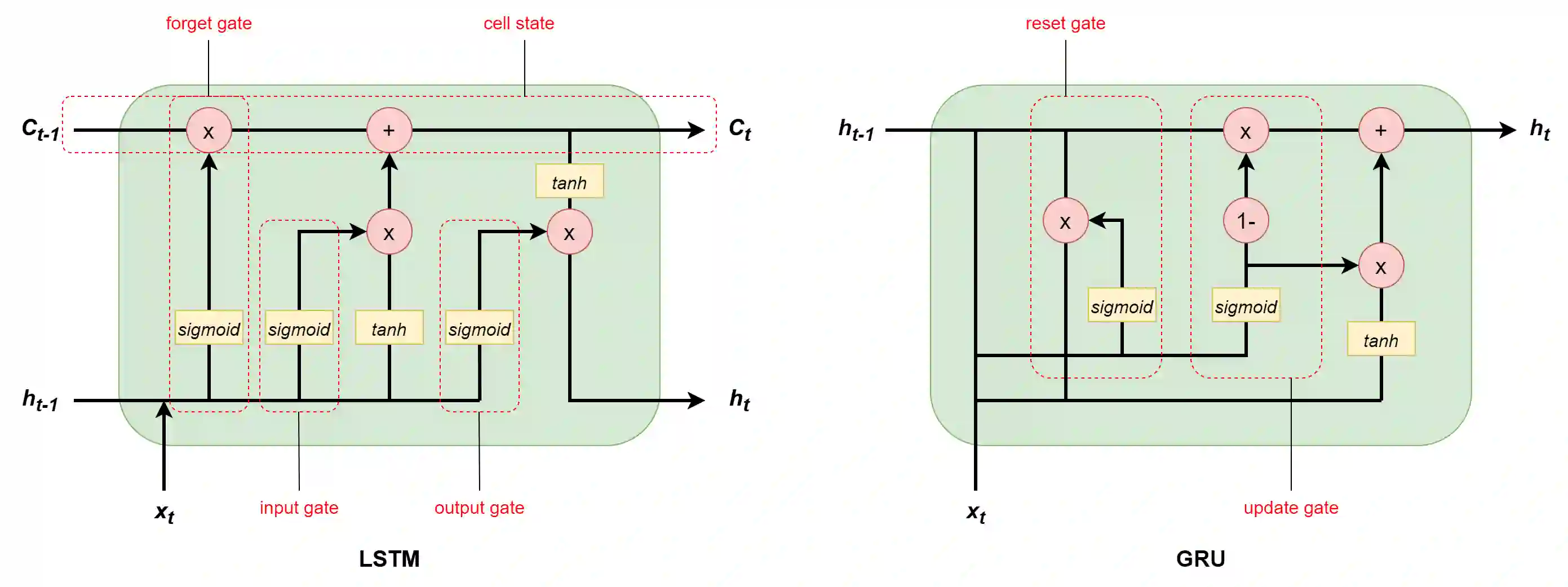

Feedforward neural network (FFN) and two specific types of recurrent neural network, long short-term memory (LSTM) and gated recurrent unit (GRU), are used for modeling US recessions in the period from 1967 to 2021. The estimated models are then employed to conduct real-time predictions of the Great Recession and the Covid-19 recession in US. Their predictive performances are compared to those of the traditional linear models, the logistic regression model both with and without the ridge penalty. The out-of-sample performance suggests the application of LSTM and GRU in the area of recession forecasting, especially for the long-term forecasting tasks. They outperform other types of models across 5 forecasting horizons with respect to different types of statistical performance metrics. Shapley additive explanations (SHAP) method is applied to the fitted GRUs across different forecasting horizons to gain insight into the feature importance. The evaluation of predictor importance differs between the GRU and ridge logistic regression models, as reflected in the variable order determined by SHAP values. When considering the top 5 predictors, key indicators such as the S\&P 500 index, real GDP, and private residential fixed investment consistently appear for short-term forecasts (up to 3 months). In contrast, for longer-term predictions (6 months or more), the term spread and producer price index become more prominent. These findings are supported by both local interpretable model-agnostic explanations (LIME) and marginal effects.

翻译:采用前馈神经网络(FFN)及两种特定类型的循环神经网络——长短期记忆网络(LSTM)与门控循环单元(GRU),对1967年至2021年间美国经济衰退进行建模。运用估算模型对美国大衰退与新冠疫情引发的经济衰退进行实时预测,并将其预测性能与传统线性模型(含/不含岭惩罚项的 logistic 回归模型)进行对比。样本外表现表明,LSTM与GRU在经济衰退预测领域具有应用价值,尤其适用于长期预测任务。在5个预测时间跨度内,两类模型基于多种统计性能指标均优于其他模型类型。采用 Shapley 加性解释(SHAP)方法对跨预测时间跨度的拟合GRU模型进行分析,以揭示特征重要性。GRU与岭 logistic 回归模型在预测因子重要性评估上存在差异,这一点体现在SHAP值决定的变量排序中。就前5个关键预测因子而言,S&P 500 指数、实际GDP及私人住宅固定投资在短期预测(3个月以内)中持续出现;而面向长期预测(6个月及以上),期限利差与生产者价格指数的重要性显著上升。上述发现得到局部可解释模型无关解释(LIME)与边际效应的双重验证。