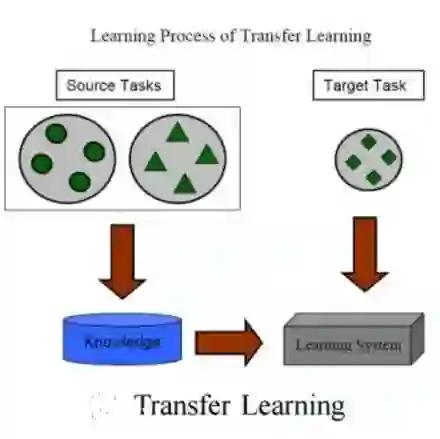

This paper introduces DeepVol, a promising new deep learning volatility model that outperforms traditional econometric models in terms of model generality. DeepVol leverages the power of transfer learning to effectively capture and model the volatility dynamics of all financial assets, including previously unseen ones, using a single universal model. This contrasts to the prevailing practice in econometrics literature, which necessitates training separate models for individual datasets. The introduction of DeepVol opens up new avenues for volatility modeling and forecasting in the finance industry, potentially transforming the way volatility is understood and predicted.

翻译:本文介绍了DeepVol,这是一种极具前景的新型深度学习波动率模型,在模型泛化能力上优于传统计量经济学模型。DeepVol利用迁移学习的优势,通过单个通用模型有效捕捉并建模所有金融资产(包括未见过的资产)的波动率动态特性。这与计量经济学文献中通行的做法(即需针对每个数据集分别训练独立模型)形成鲜明对比。DeepVol的引入为金融行业的波动率建模与预测开辟了新途径,有望从根本上改变人们对波动率的理解与预测方式。