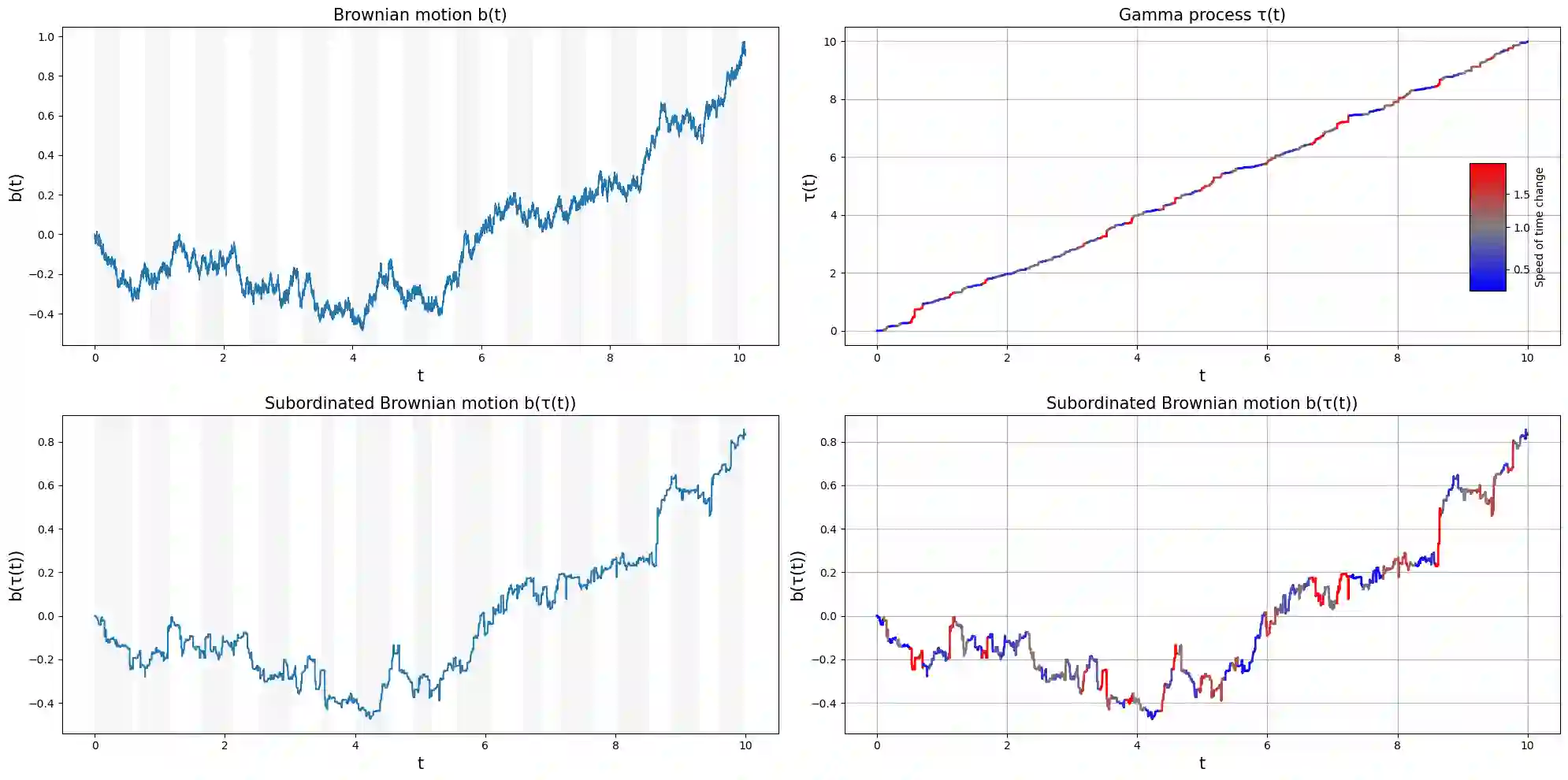

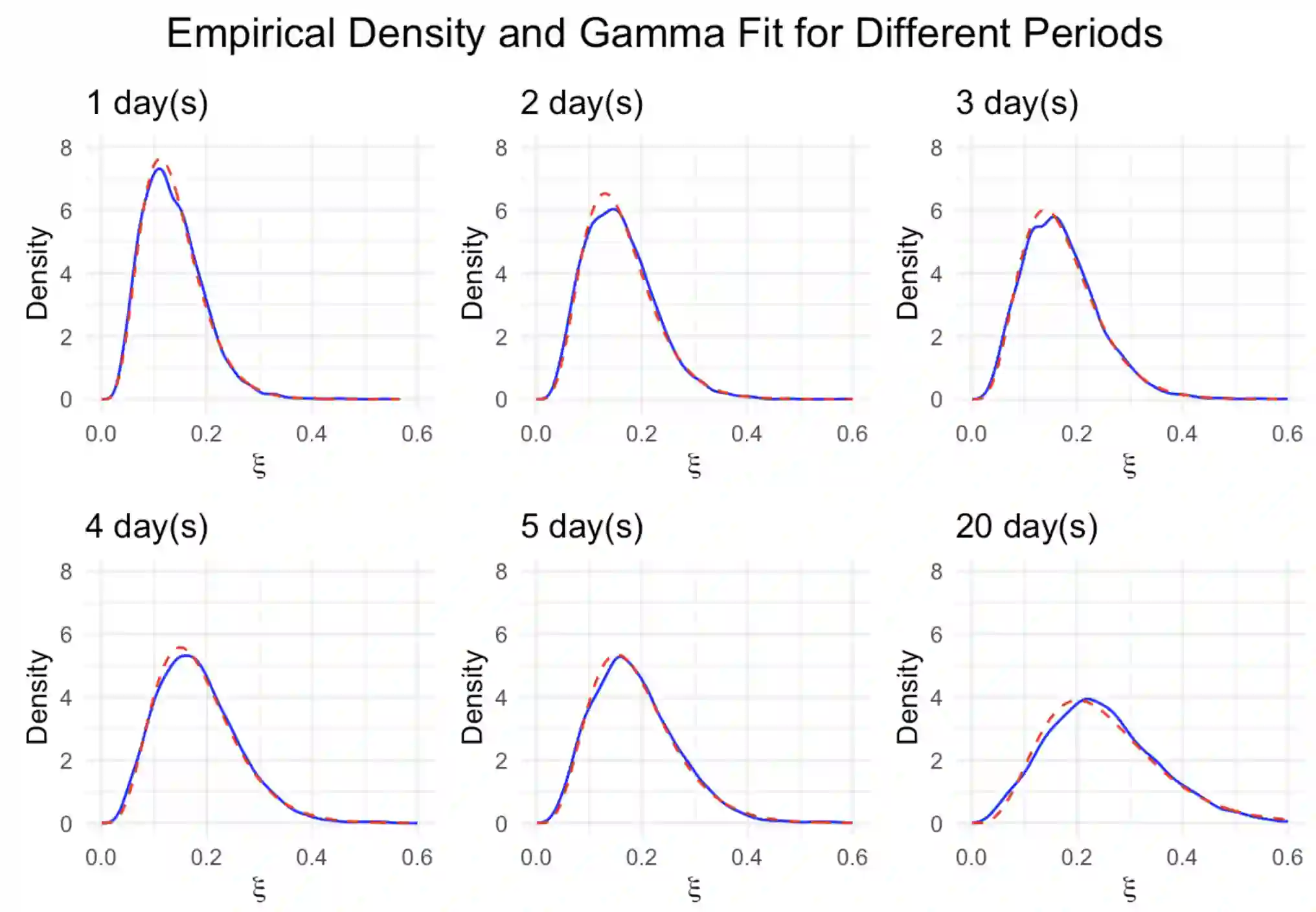

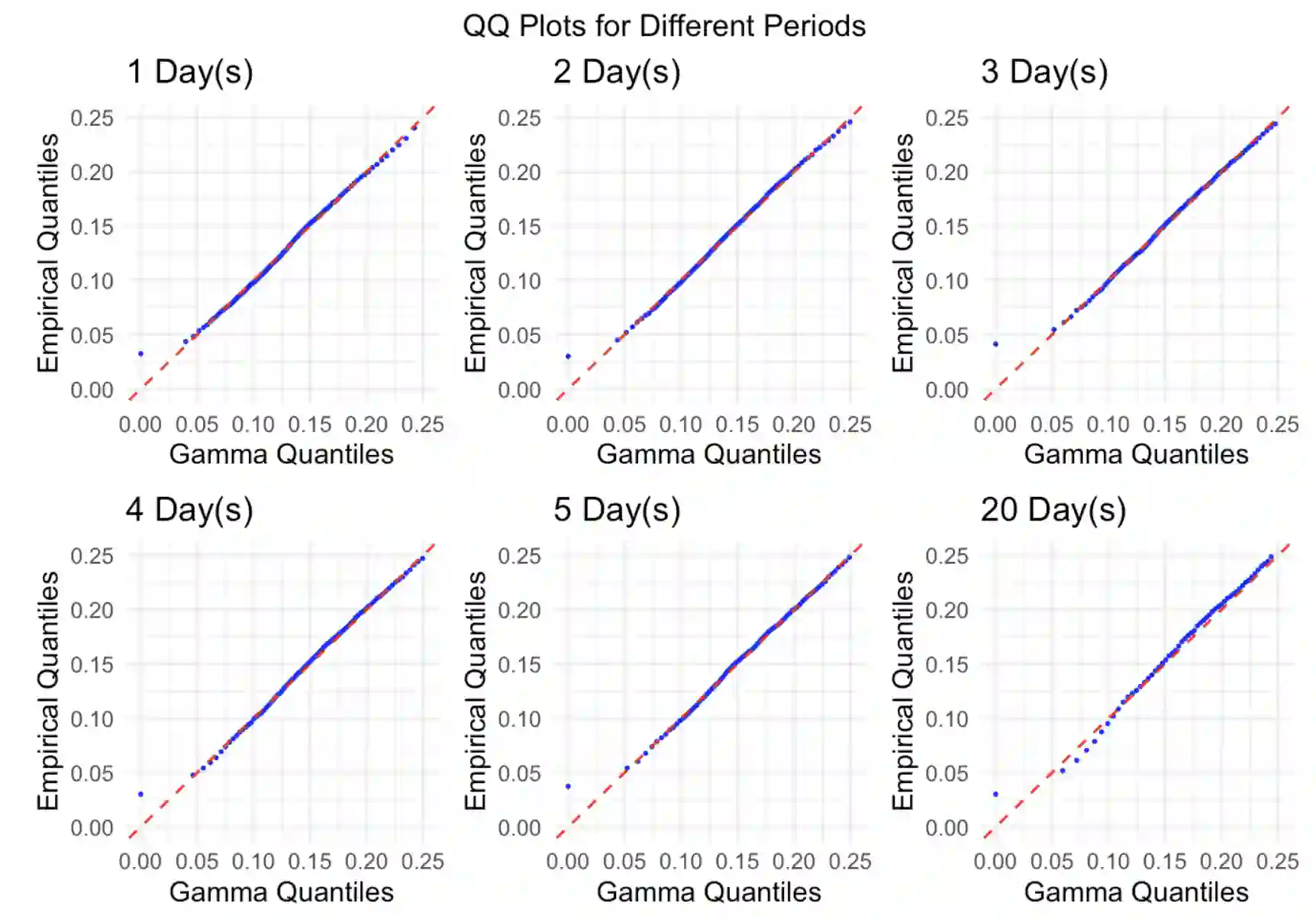

In the context of time-subordinated Brownian motion models, Fourier theory and methodology are proposed to modelling the stochastic distribution of time increments. Gaussian Variance-Mean mixtures and time-subordinated models are reviewed with a key example being the Variance-Gamma process. A non-parametric characteristic function decomposition of subordinated Brownian motion is presented. The theory requires an extension of the real domain of certain characteristic functions to the complex plane, the validity of which is proven here. This allows one to characterise and study the stochastic time-change directly from the full process. An empirical decomposition of S\&P log-returns is provided to illustrate the methodology.

翻译:在时从属布朗运动模型的背景下,本文提出利用傅里叶理论和方法来建模时间增量的随机分布。文中回顾了高斯方差-均值混合模型及时从属模型,并以方差-伽马过程作为关键示例。提出了一种时从属布朗运动的非参数特征函数分解方法。该理论要求将某些特征函数的实数域扩展至复平面,本文证明了这种扩展的有效性。这使得研究者能够直接从完整过程出发来刻画和研究随机时间变换。文中提供了标准普尔对数收益率的经验分解以说明该方法。