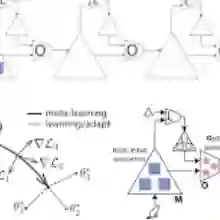

Natural language understanding(NLU) is challenging for finance due to the lack of annotated data and the specialized language in that domain. As a result, researchers have proposed to use pre-trained language model and multi-task learning to learn robust representations. However, aggressive fine-tuning often causes over-fitting and multi-task learning may favor tasks with significantly larger amounts data, etc. To address these problems, in this paper, we investigate model-agnostic meta-learning algorithm(MAML) in low-resource financial NLU tasks. Our contribution includes: 1. we explore the performance of MAML method with multiple types of tasks: GLUE datasets, SNLI, Sci-Tail and Financial PhraseBank; 2. we study the performance of MAML method with multiple single-type tasks: a real scenario stock price prediction problem with twitter text data. Our models achieve the state-of-the-art performance according to the experimental results, which demonstrate that our method can adapt fast and well to low-resource situations.

翻译:自然语言理解在金融领域极具挑战性,原因在于该领域缺乏标注数据且存在专业语言现象。为此,研究者提出了使用预训练语言模型和多任务学习方法来学习鲁棒性表征。然而,激进微调常导致过拟合,多任务学习可能偏向数据量显著更大的任务。针对这些问题,本文研究了低资源金融自然语言理解任务中的模型无关元学习算法。我们的贡献包括:1. 探索了MAML方法在包含GLUE数据集、SNLI、Sci-Tail和金融短语库的多类型任务上的性能;2. 研究了MAML方法在单一类型多任务(基于推文文本数据的真实场景股价预测问题)上的性能。实验结果表明,我们的模型达到了最先进的性能,证明该方法能快速且良好地适应低资源场景。