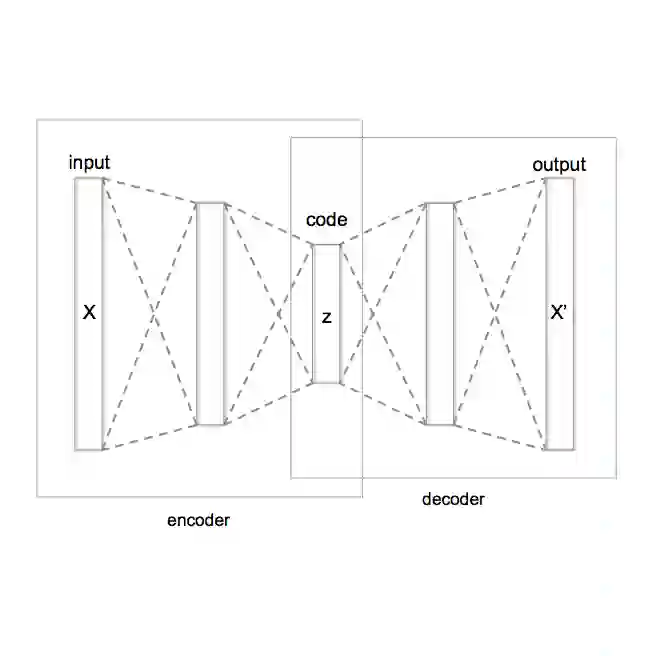

Missing data is a common problem in finance and often requires methods to fill in the gaps, or in other words, imputation. In this work, we focused on the imputation of missing implied volatilities for FX options. Prior work has used variational autoencoders (VAEs), a neural network-based approach, to solve this problem; however, using stronger classical baselines such as Heston with jumps can significantly outperform their results. We show that simple modifications to the architecture of the VAE lead to significant imputation performance improvements (e.g., in low missingness regimes, nearly cutting the error by half), removing the necessity of using $\beta$-VAEs. Further, we modify the VAE imputation algorithm in order to better handle the uncertainty in data, as well as to obtain accurate uncertainty estimates around imputed values.

翻译:在金融领域,数据缺失是一个普遍存在的问题,通常需要采用填补空白的方法,即插补技术。本研究聚焦于外汇期权隐含波动率缺失值的插补问题。先前的研究已使用变分自编码器(VAE)这一基于神经网络的方法来解决该问题;然而,采用更强大的经典基线模型(如带跳跃的Heston模型)可显著超越其插补效果。我们证明,通过对VAE架构进行简单修改,即可显著提升插补性能(例如在低缺失率情况下,误差可降低近半),从而无需使用$\beta$-VAE。此外,我们改进了VAE插补算法,以更好地处理数据中的不确定性,并获取插补值周围更准确的不确定性估计。