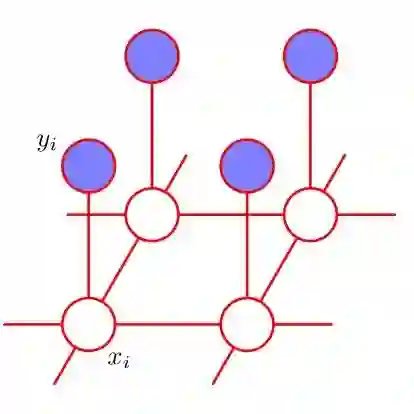

We propose risk models for a portfolio of risks, each following a compound Poisson distribution, with dependencies introduced through a family of tree-based Markov random fields with Poisson marginal distributions inspired in C\^ot\'e et al. (2024b, arXiv:2408.13649). The diversity of tree topologies allows for the construction of risk models under several dependence schemes. We study the distribution of the random vector of risks and of the aggregate claim amount of the portfolio. We perform two risk management tasks: the assessment of the global risk of the portfolio and its allocation to each component. Numerical examples illustrate the findings and the efficiency of the computation methods developed throughout. We also show that the discussed family of Markov random fields is a subfamily of the multivariate Poisson distribution constructed through common shocks.

翻译:我们针对一组风险组合提出风险模型,其中每个风险服从复合泊松分布,其相依性通过一系列基于树的马尔可夫随机场引入,该随机场的边缘分布为泊松分布,其设计灵感来源于C\^ot\'e等人(2024b, arXiv:2408.13649)的工作。树拓扑结构的多样性使得我们能够在多种相依性方案下构建风险模型。我们研究了风险随机向量及组合总索赔额的分布。我们执行了两项风险管理任务:评估组合的整体风险并将其分配到各个组成部分。数值算例阐释了研究结果以及本文所开发计算方法的效率。我们还证明了所讨论的马尔可夫随机场族是通过共同冲击构建的多元泊松分布的一个子族。