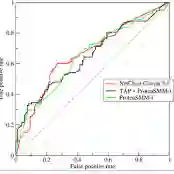

The high-frequency issuance and short-cycle speculation of meme tokens in decentralized finance (DeFi) have significantly amplified rug-pull risk. Existing approaches still struggle to provide stable early warning under scarce anomalies, incomplete labels, and limited interpretability. To address this issue, an end-to-end warning framework is proposed for BSC meme tokens, consisting of four stages: dataset construction and labeling, wash-trading pattern feature modeling, risk prediction, and error analysis. Methodologically, 12 token-level behavioral features are constructed based on three wash-trading patterns (Self, Matched, and Circular), unifying transaction-, address-, and flow-level signals into risk vectors. Supervised models are then employed to output warning scores and alert decisions. Under the current setting (7 tokens, 33,242 records), Random Forest outperforms Logistic Regression on core metrics, achieving AUC=0.9098, PR-AUC=0.9185, and F1=0.7429. Ablation results show that trade-level features are the primary performance driver (Delta PR-AUC=-0.1843 when removed), while address-level features provide stable complementary gain (Delta PR-AUC=-0.0573). The model also demonstrates actionable early-warning potential for a subset of samples, with a mean Lead Time (v1) of 3.8133 hours. The error profile (FP=1, FN=8) indicates that the current system is better positioned as a high-precision screener rather than a high-recall automatic alarm engine. The main contributions are threefold: an executable and reproducible rug-pull warning pipeline, empirical validation of multi-granularity wash-trading features under weak supervision, and deployment-oriented evidence through lead-time and error-bound analysis.

翻译:去中心化金融(DeFi)中模因代币的高频发行与短周期投机行为,显著放大了拉地毯(rug-pull)风险。现有方法在异常样本稀缺、标签不完整及可解释性有限的情况下,仍难以提供稳定的早期预警。为解决此问题,本文提出一个面向BSC模因代币的端到端预警框架,包含四个阶段:数据集构建与标注、对敲交易模式特征建模、风险预测及误差分析。在方法论上,基于三种对敲交易模式(自成交、匹配成交与循环成交),构建了12个代币级别的行为特征,将交易级、地址级与资金流级信号统一为风险向量。随后采用监督模型输出预警分数与警报决策。在当前设定(7个代币,33,242条记录)下,随机森林在核心指标上优于逻辑回归,实现了AUC=0.9098、PR-AUC=0.9185与F1=0.7429。消融实验结果表明,交易级特征是性能的主要驱动力(移除后Delta PR-AUC=-0.1843),而地址级特征提供了稳定的补充增益(Delta PR-AUC=-0.0573)。该模型对部分样本亦展现出可操作的早期预警潜力,平均前置时间(v1)为3.8133小时。误差分布(FP=1,FN=8)表明,当前系统更适合定位为高精度筛查器,而非高召回率的自动警报引擎。主要贡献包括三方面:一个可执行、可复现的拉地毯预警流程;在弱监督下对多粒度对敲交易特征进行的实证验证;以及通过前置时间与误差边界分析提供的面向部署的证据。