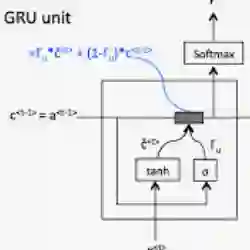

This document presents an in-depth examination of stock market sentiment through the integration of Convolutional Neural Networks (CNN) and Gated Recurrent Units (GRU), enabling precise risk alerts. The robust feature extraction capability of CNN is utilized to preprocess and analyze extensive network text data, identifying local features and patterns. The extracted feature sequences are then input into the GRU model to understand the progression of emotional states over time and their potential impact on future market sentiment and risk. This approach addresses the order dependence and long-term dependencies inherent in time series data, resulting in a detailed analysis of stock market sentiment and effective early warnings of future risks.

翻译:本文通过整合卷积神经网络(CNN)与门控循环单元(GRU),对股市情绪进行深入研究,以实现精准的风险预警。利用CNN强大的特征提取能力,对海量网络文本数据进行预处理与分析,识别局部特征与模式。随后,将提取的特征序列输入GRU模型,以理解情绪状态随时间的演变过程及其对未来市场情绪与风险的潜在影响。该方法解决了时间序列数据固有的顺序依赖性与长期依赖问题,从而实现了对股市情绪的细致分析,并对未来风险进行了有效的早期预警。