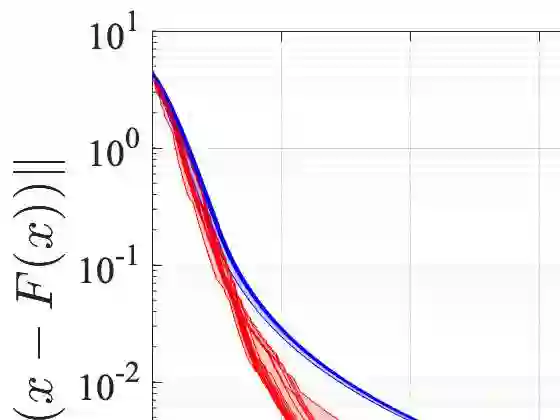

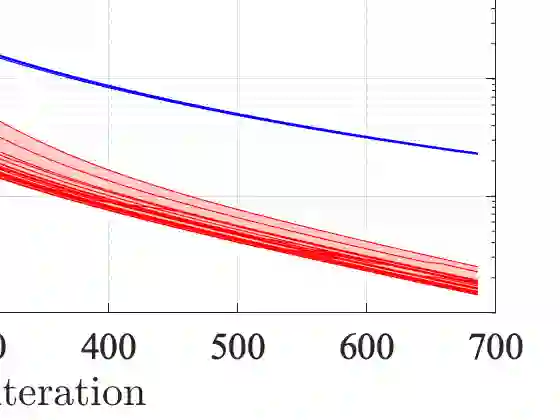

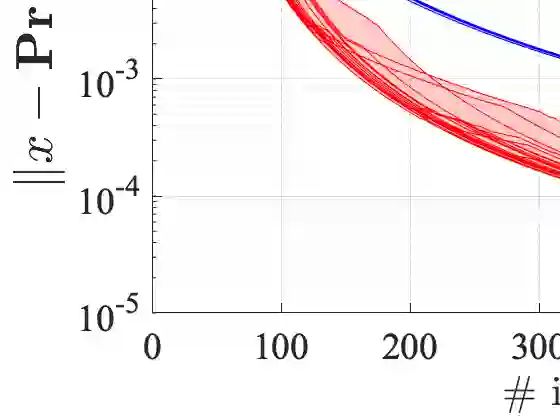

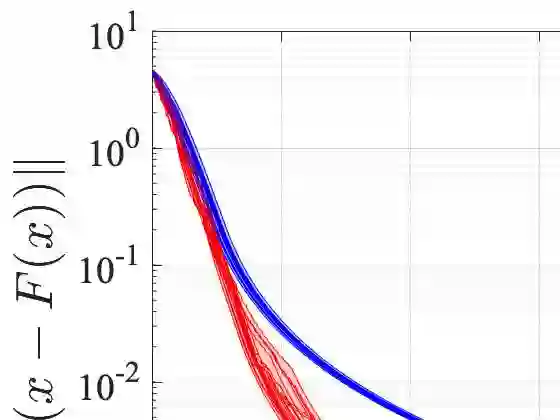

We consider a class of Wasserstein distributionally robust Nash equilibrium problems, where agents construct heterogeneous data-driven Wasserstein ambiguity sets using private samples and radii, in line with their individual risk-averse behaviour. By leveraging relevant properties of this class of games, we show that equilibria of the original seemingly infinite-dimensional problem can be obtained as a solution to a finite-dimensional Nash equilibrium problem. We then reformulate the problem as a finite-dimensional variational inequality and establish the connection between the corresponding solution sets. Our reformulation has scalable behaviour with respect to the data size and maintains a fixed number of constraints, independently of the number of samples. To compute a solution, we leverage two algorithms, based on the golden ratio algorithm. The efficiency of both algorithmic schemes is corroborated through extensive simulation studies on an illustrative example and a stochastic portfolio allocation game, where behavioural coupling among investors is modeled.

翻译:本文研究一类Wasserstein分布鲁棒纳什均衡问题,其中各智能体根据其个体风险规避行为,利用私有样本和半径构建异构的数据驱动Wasserstein模糊集。通过利用此类博弈的相关性质,我们证明原始看似无限维问题的均衡解可通过求解有限维纳什均衡问题获得。随后我们将该问题重构为有限维变分不等式,并建立相应解集之间的关联。我们的重构方法在数据规模上具有可扩展性,且约束条件数量固定,与样本数量无关。为求解该问题,我们基于黄金分割算法提出了两种计算方案。通过在示例性算例和随机投资组合配置博弈(其中建模了投资者间的行为耦合)上进行大量仿真研究,验证了两种算法方案的有效性。