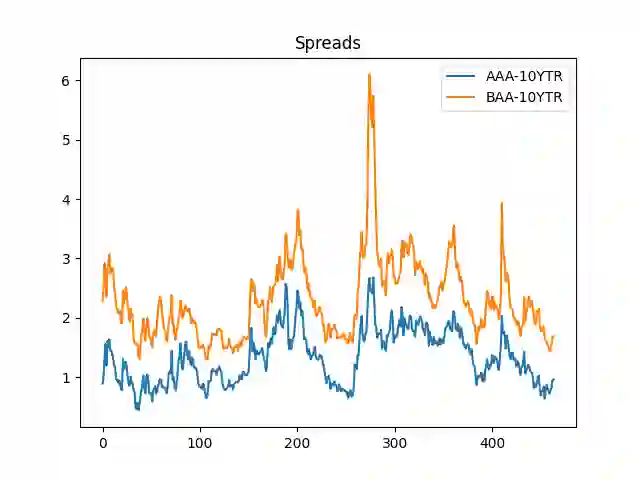

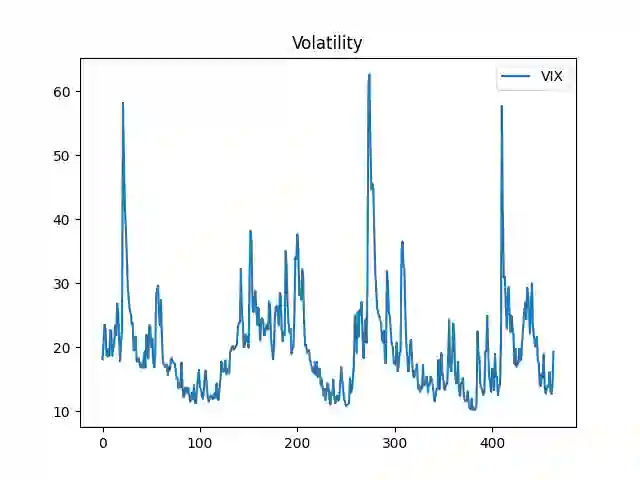

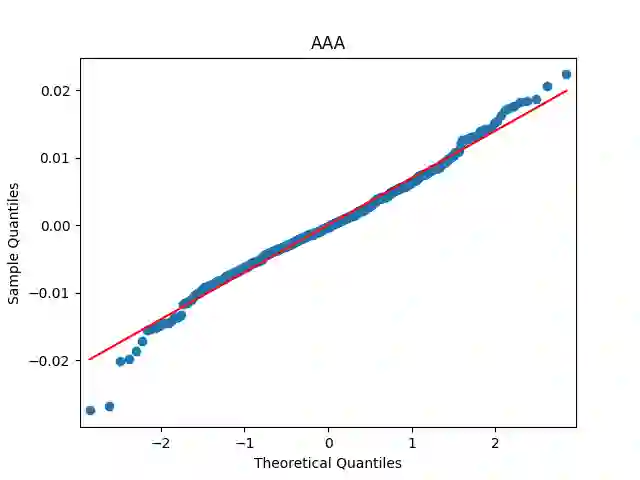

Classic stochastic volatility models assume volatility is unobservable. We use the VIX for consider it observable, and use the Volatility Index: S\&P 500 VIX. This index was designed to measure volatility of S&P 500. We apply it to a different segment: Corporate bond markets. We fit time series models for spreads between corporate and 10-year Treasury bonds. Next, we divide residuals by VIX. Our main idea is such division makes residuals closer to the ideal case of a Gaussian white noise. This is remarkable, since these residuals and VIX come from separate market segments. We also discuss total returns of Bank of America corporate bonds. We conclude with the analysis of long-term behavior of these models.

翻译:经典随机波动率模型假设波动率不可观测。我们通过引入VIX指数将其视为可观测变量,具体采用标准普尔500波动率指数(S&P 500 VIX)。该指数原为衡量标普500指数波动率而设计,本文将其应用于不同市场领域:公司债券市场。我们构建了公司债券与10年期国债利差的时间序列模型,随后将模型残差除以VIX值。核心创新在于:该除法运算能使残差更接近理想的高斯白噪声状态,这一现象尤为显著,因为残差与VIX源自相互独立的市场领域。本文进一步探讨美国银行公司债券的总回报表现,最后对这些模型的长期行为特征进行分析。