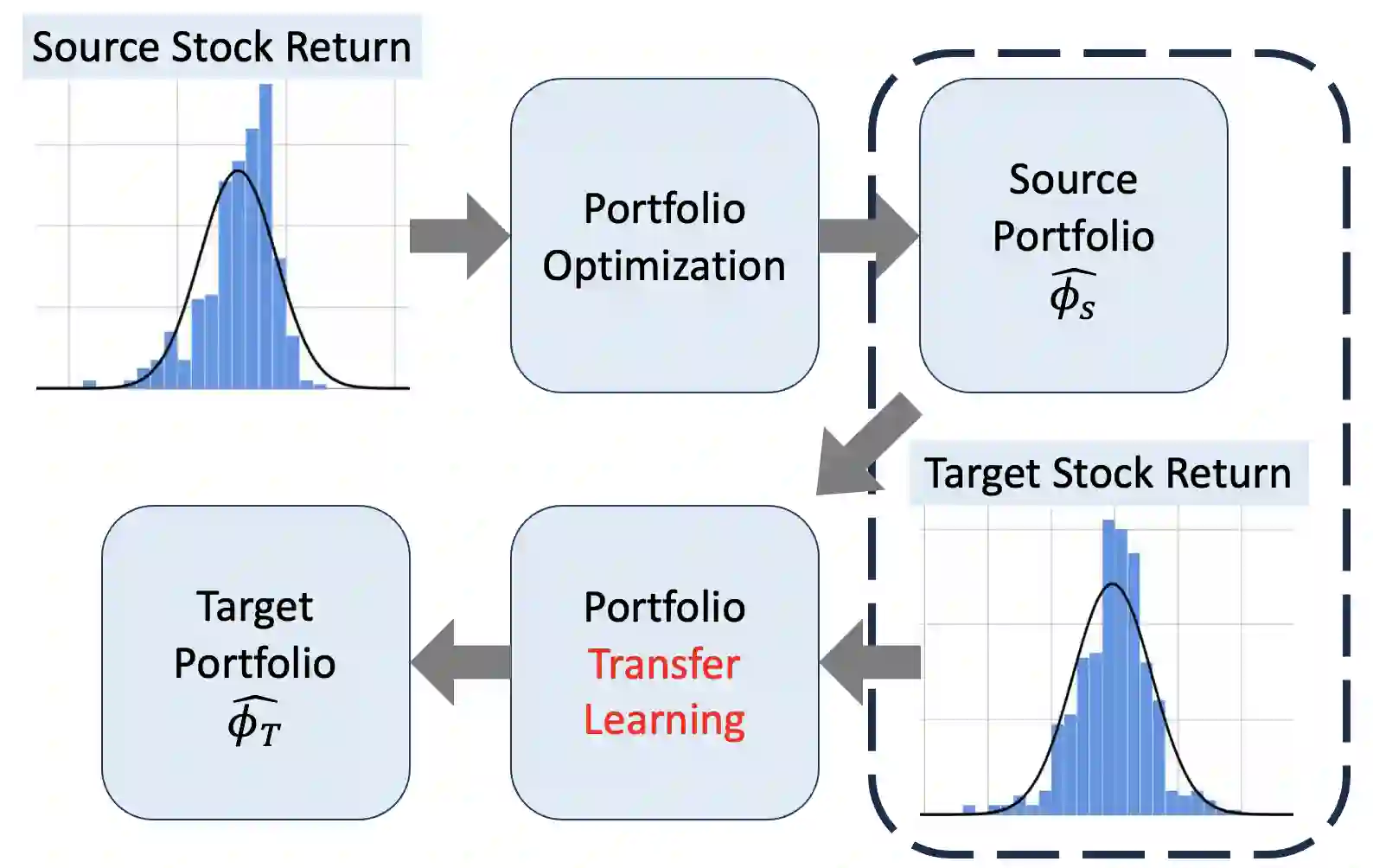

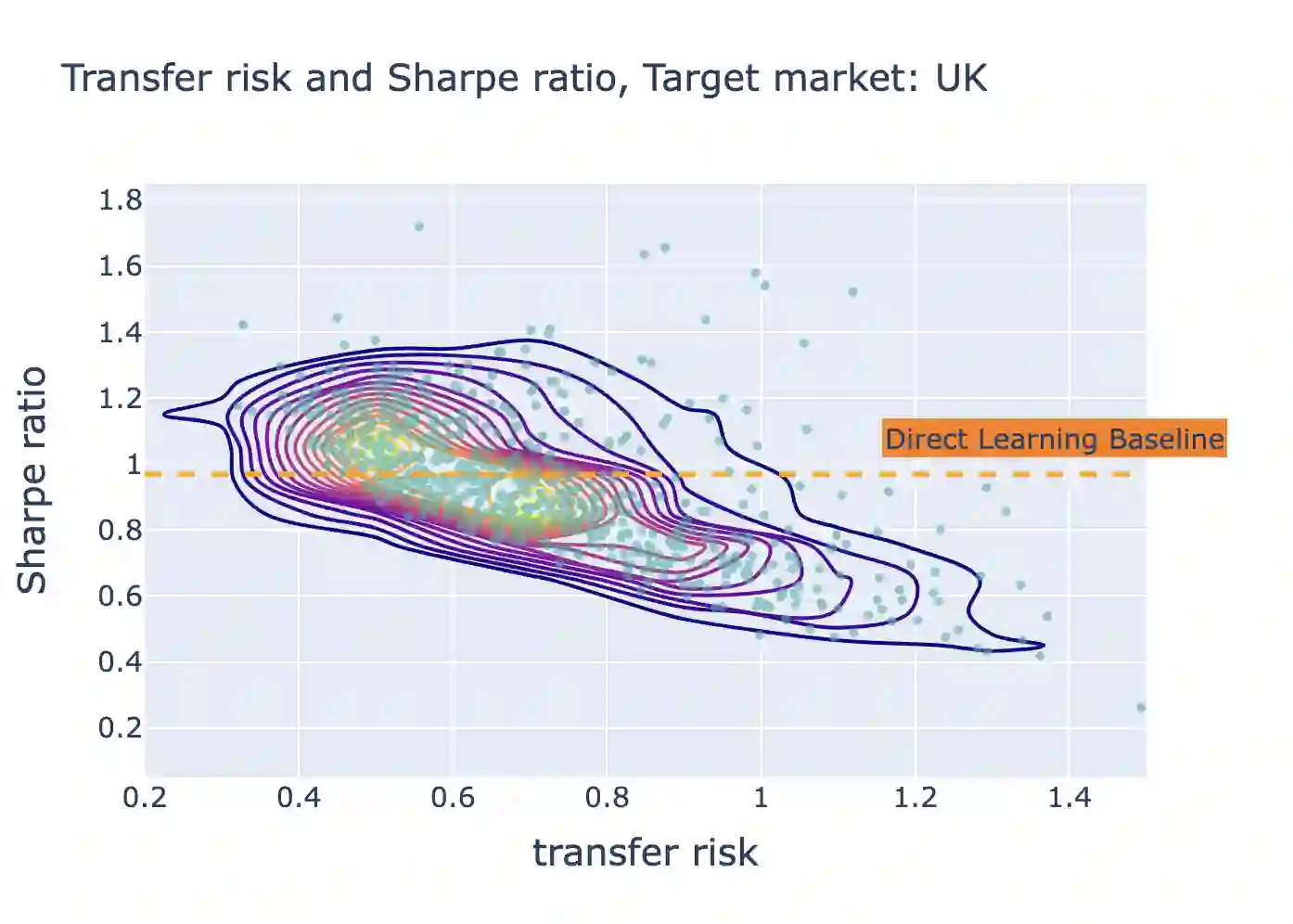

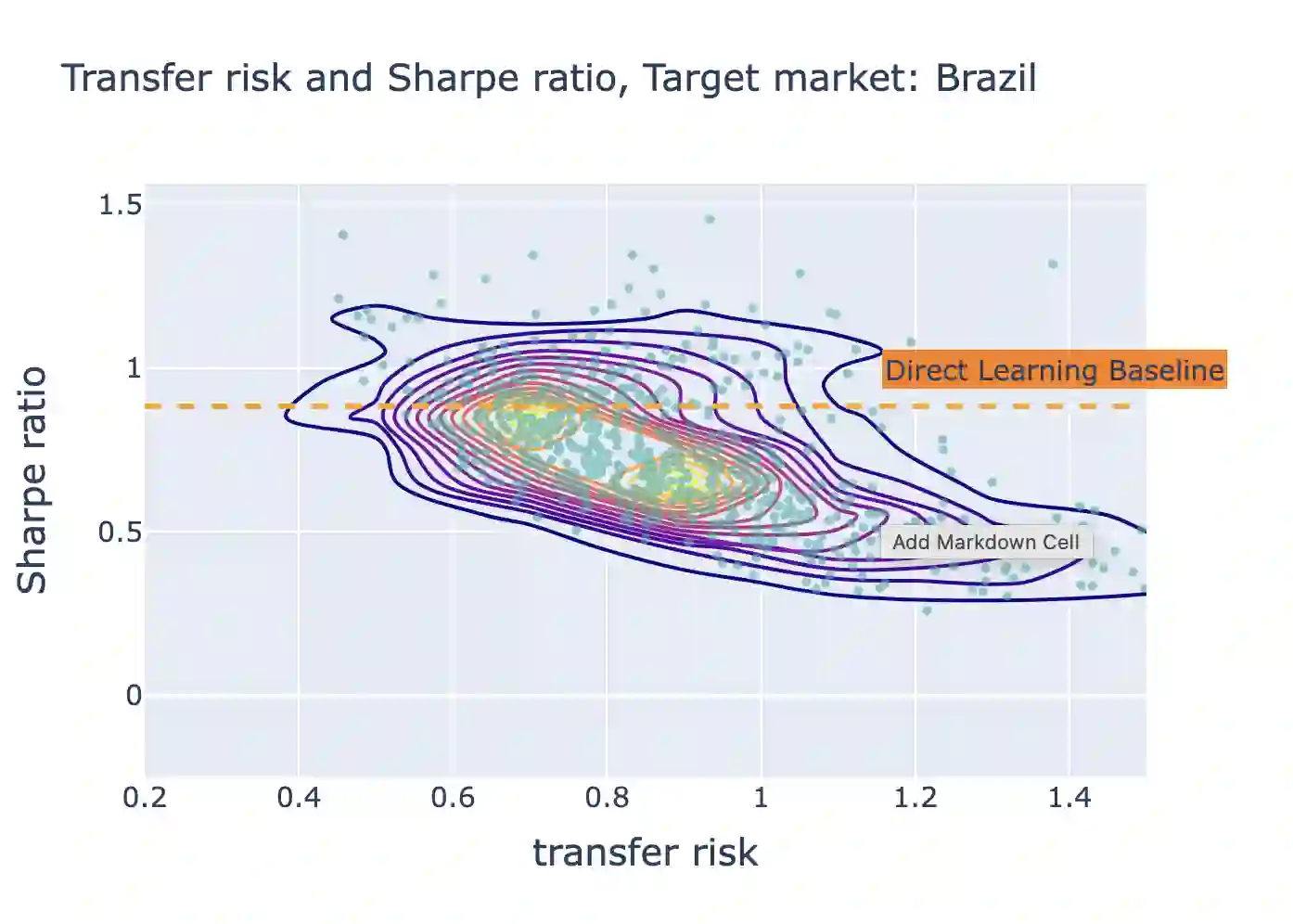

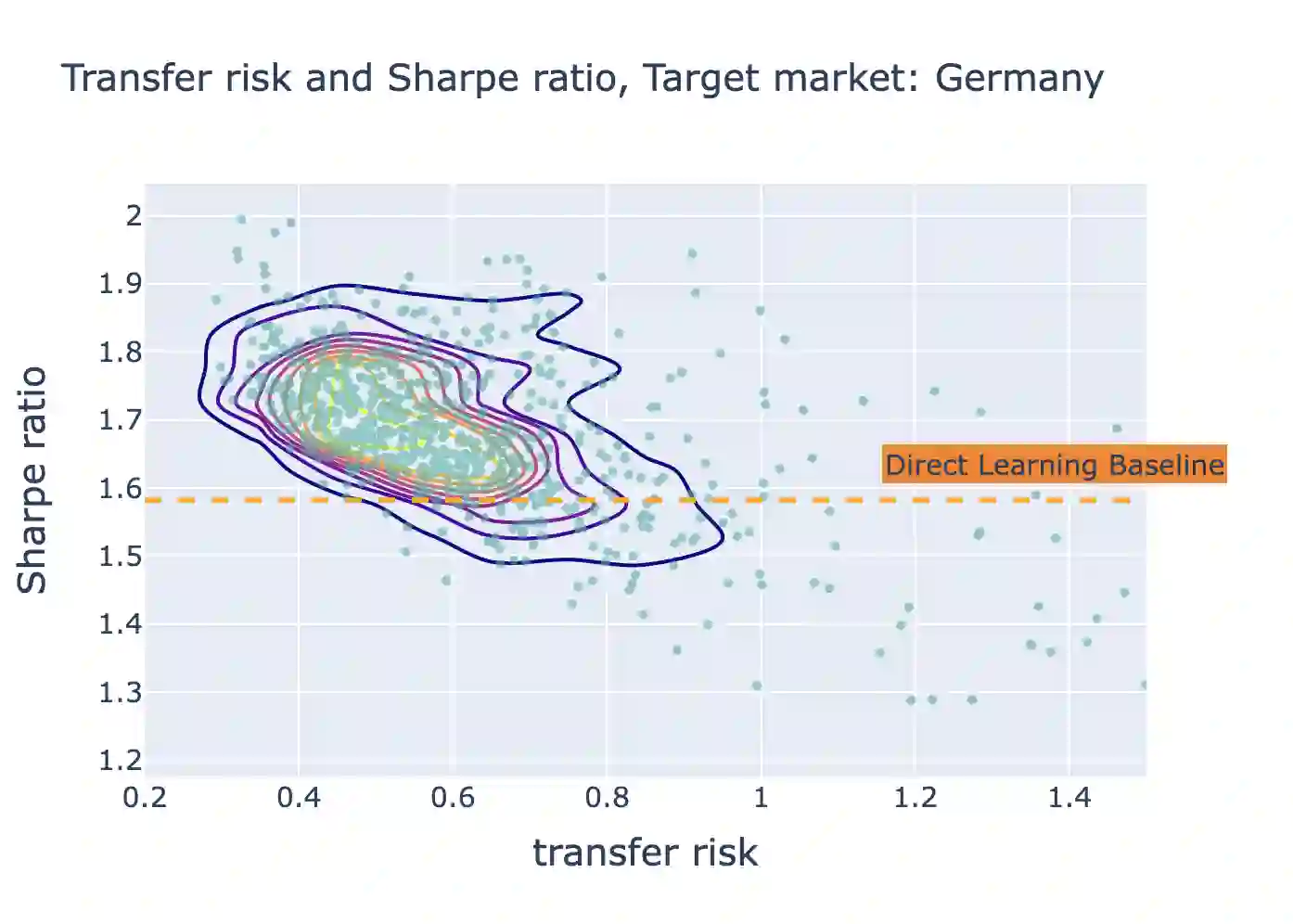

In this work, we explore the possibility of utilizing transfer learning techniques to address the financial portfolio optimization problem. We introduce a novel concept called "transfer risk", within the optimization framework of transfer learning. A series of numerical experiments are conducted from three categories: cross-continent transfer, cross-sector transfer, and cross-frequency transfer. In particular, 1. a strong correlation between the transfer risk and the overall performance of transfer learning methods is established, underscoring the significance of transfer risk as a viable indicator of "transferability"; 2. transfer risk is shown to provide a computationally efficient way to identify appropriate source tasks in transfer learning, enhancing the efficiency and effectiveness of the transfer learning approach; 3. additionally, the numerical experiments offer valuable new insights for portfolio management across these different settings.

翻译:在本文中,我们探索了利用迁移学习技术解决金融投资组合优化问题的可能性。我们在迁移学习的优化框架内引入了一个名为“迁移风险”的新概念。通过三类数值实验(跨地区迁移、跨行业迁移和跨频率迁移)展开研究。具体而言:1. 迁移风险与迁移学习方法整体表现之间存在强相关性,证实了迁移风险作为“可迁移性”有效指标的显著意义;2. 迁移风险被证明能为迁移学习中源任务的筛选提供一种高效计算方法,从而提升迁移学习方法的效能与效率;3. 此外,这些数值实验为上述不同场景下的投资组合管理提供了有价值的新见解。