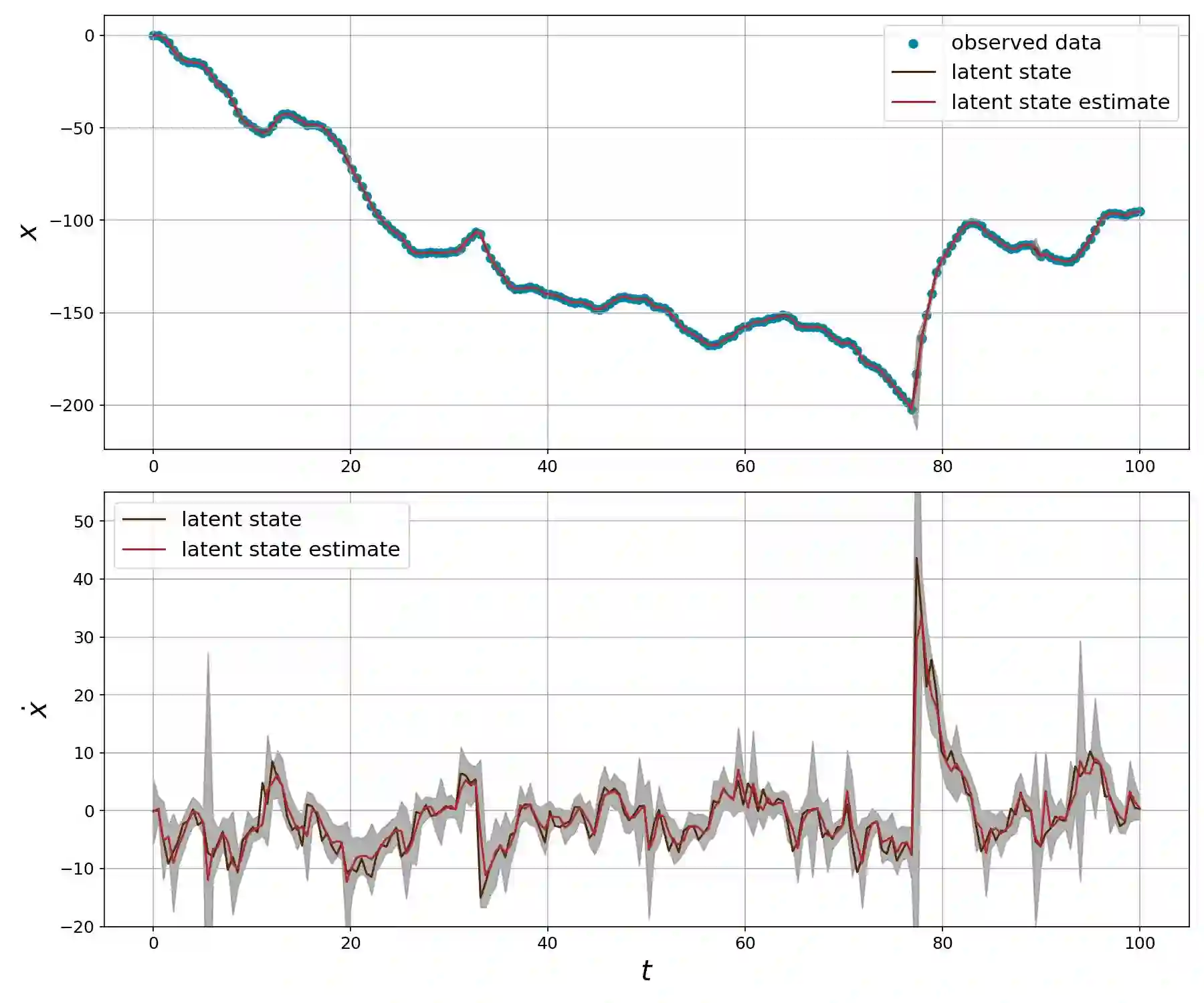

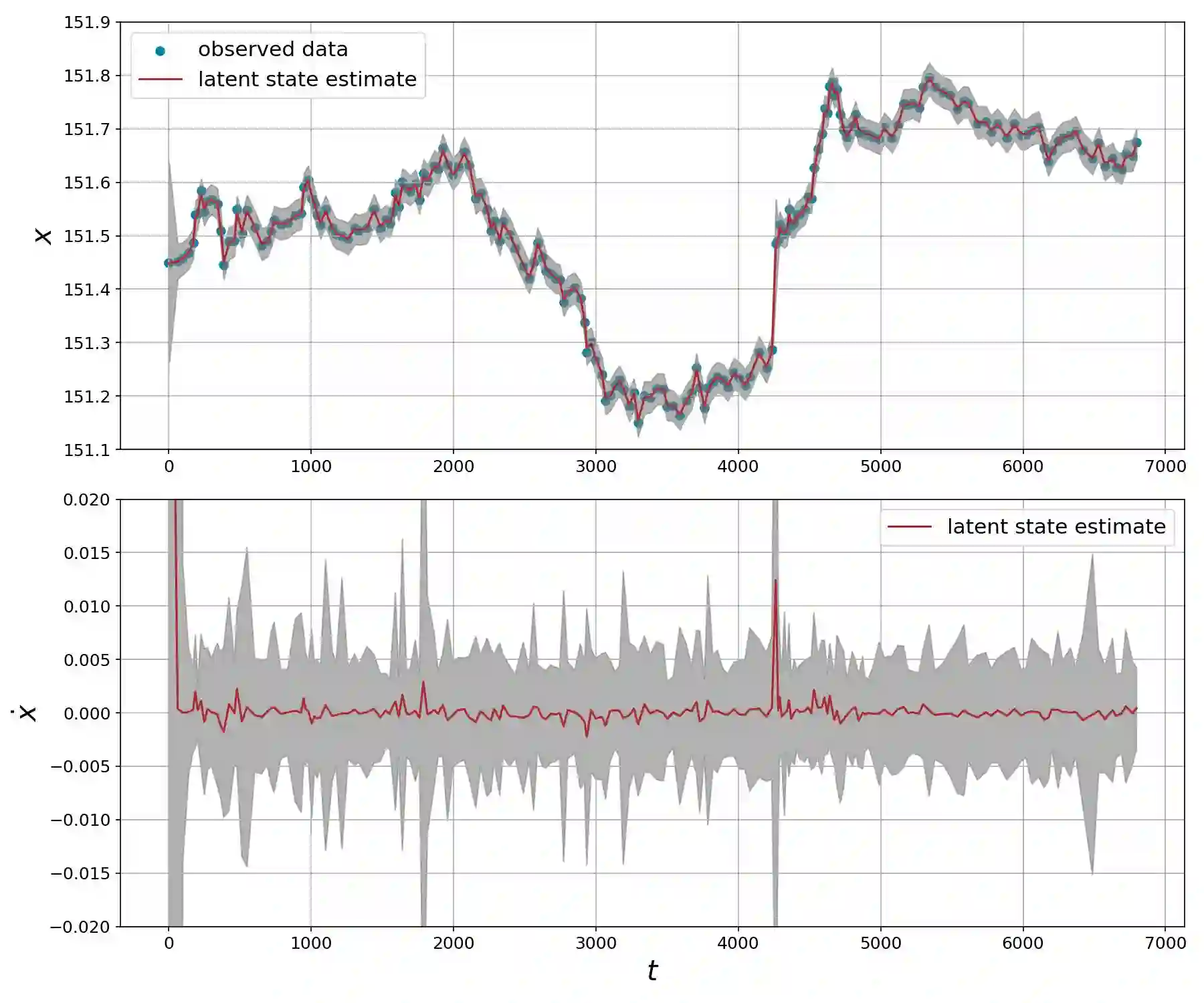

In this work we study linear vector stochastic differential equation (SDE) models driven by the generalised hyperbolic (GH) L\'evy process for inference in continuous-time non-Gaussian filtering problems. The GH family of stochastic processes offers a flexible framework for modelling of non-Gaussian, heavy-tailed characteristics and includes the normal inverse-Gaussian, variance-gamma and Student-t processes as special cases. We present continuous-time simulation methods for the solution of vector SDE models driven by GH processes and novel inference methodologies using a variant of sequential Markov chain Monte Carlo (MCMC). As an example a particular formulation of Langevin dynamics is studied within this framework. The model is applied to both a synthetically generated data set and a real-world financial series to demonstrate its capabilities.

翻译:本文研究了由广义双曲(GH)Lévy过程驱动的线性向量随机微分方程(SDE)模型,用于连续时间非高斯滤波问题中的推理。GH随机过程族为非高斯、重尾特征建模提供了灵活的框架,其中包括正态逆高斯过程、方差伽马过程和学生t过程作为特例。我们提出了用于求解由GH过程驱动的向量SDE模型的连续时间模拟方法,以及利用序贯马尔可夫链蒙特卡洛(MCMC)变体的新型推理方法。作为示例,在该框架下研究了特定形式的朗之万动力学。该模型被应用于合成生成的数据集和实际金融序列,以展示其能力。