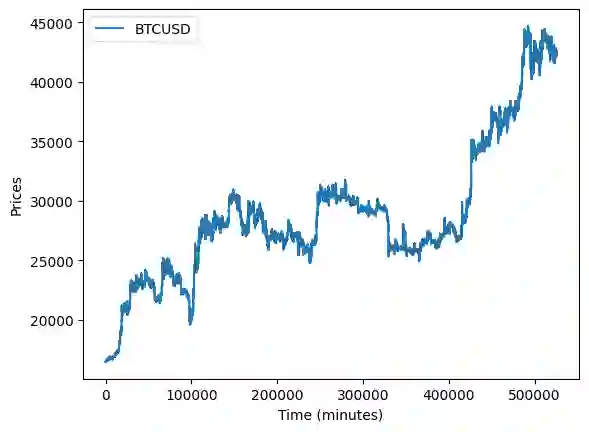

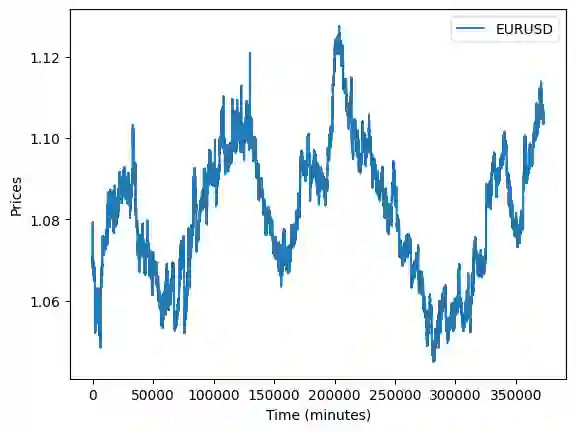

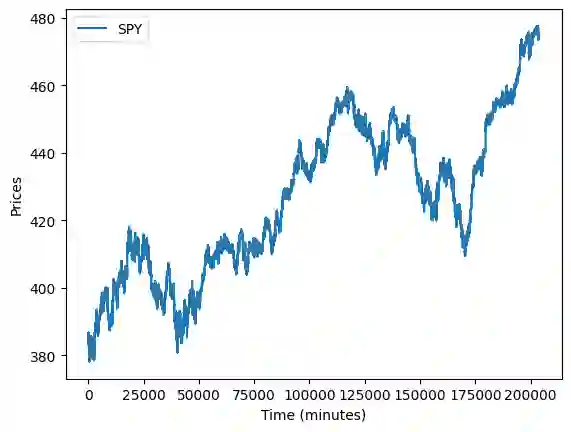

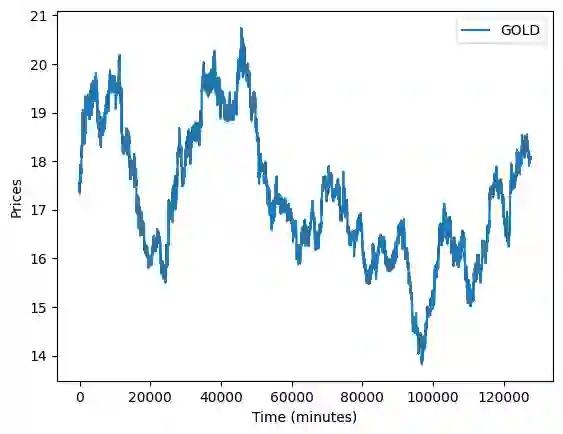

The Pairwise Markov Chain (PMC) is a probabilistic graphical model extending the well-known Hidden Markov Model. This model, although highly effective for many tasks, has been scarcely utilized for continuous value prediction. This is mainly due to the issue of modeling observations inherent in generative probabilistic models. In this paper, we introduce a new algorithm for prediction with the PMC. On the one hand, this algorithm allows circumventing the feature problem, thus fully exploiting the capabilities of the PMC. On the other hand, it enables the PMC to extend any predictive model by introducing hidden states, updated at each time step, and allowing the introduction of non-stationarity for any model. We apply the PMC with its new algorithm for volatility forecasting, which we compare to the highly popular GARCH(1,1) and feedforward neural models across numerous pairs. This is particularly relevant given the regime changes that we can observe in volatility. For each scenario, our algorithm enhances the performance of the extended model, demonstrating the value of our approach.

翻译:成对马尔可夫链(PMC)是一种扩展了经典隐马尔可夫模型的概率图模型。该模型虽然在众多任务中表现出色,却极少被用于连续值预测,这主要源于生成式概率模型固有的观测建模问题。本文提出了一种基于PMC的新预测算法:一方面,该算法能够规避特征建模难题,从而充分发挥PMC的潜力;另一方面,PMC可通过引入隐藏状态(每个时间步动态更新)来扩展任意预测模型,并为任何模型引入非平稳性处理能力。我们将搭载新算法的PMC应用于波动率预测,并在多组数据对上与广泛使用的GARCH(1,1)模型及前馈神经网络模型进行比较。鉴于波动率中可观测到的状态转换现象,这一研究具有重要意义。实验表明,在所有测试场景中,新算法均能提升扩展模型的预测性能,验证了本方法的实用价值。