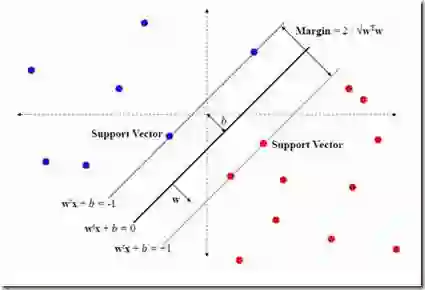

Economic models produce moment inequalities, which can be used to form tests of the true parameters. Confidence sets (CS) of the true parameters are derived by inverting these tests. However, they often lack analytical expressions, necessitating a grid search to obtain the CS numerically by retaining the grid points that pass the test. When the statistic is not asymptotically pivotal, constructing the critical value for each grid point in the parameter space adds to the computational burden. In this paper, we convert the computational issue into a classification problem by using a support vector machine (SVM) classifier. Its decision function provides a faster and more systematic way of dividing the parameter space into two regions: inside vs. outside of the confidence set. We label those points in the CS as 1 and those outside as -1. Researchers can train the SVM classifier on a grid of manageable size and use it to determine whether points on denser grids are in the CS or not. We establish certain conditions for the grid so that there is a tuning that allows us to asymptotically reproduce the test in the CS. This means that in the limit, a point is classified as belonging to the confidence set if and only if it is labeled as 1 by the SVM.

翻译:经济模型产生矩不等式,可用于构建真实参数的检验。通过反转这些检验可推导出真实参数的置信集。然而,置信集通常缺乏解析表达式,需要通过网格搜索保留通过检验的网格点来数值化获取置信集。当统计量非渐近枢轴时,为参数空间中每个网格点构建临界值会进一步增加计算负担。本文通过使用支持向量机分类器将计算问题转化为分类问题。其决策函数提供了一种更快速、更系统化的方法,将参数空间划分为两个区域:置信集内部与外部。我们将置信集内的点标记为1,外部点标记为-1。研究者可在可控规模的网格上训练SVM分类器,并利用其判断更密集网格上的点是否属于置信集。我们为网格建立了特定条件,使得通过参数调优能够渐近复现置信集中的检验。这意味着在极限情况下,当且仅当某点被SVM标记为1时,该点被分类为属于置信集。