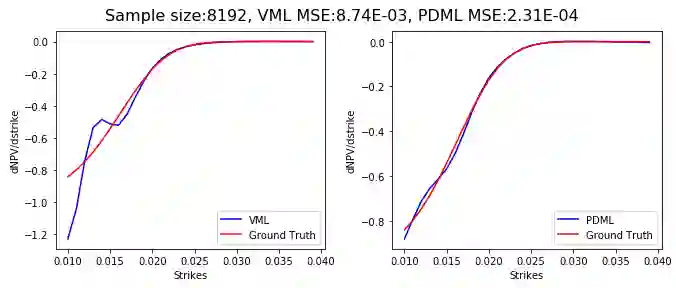

Differential machine learning (DML) is a recently proposed technique that uses samplewise state derivatives to regularize least square fits to learn conditional expectations of functionals of stochastic processes as functions of state variables. Exploiting the derivative information leads to fewer samples than a vanilla ML approach for the same level of precision. This paper extends the methodology to parametric problems where the processes and functionals also depend on model and contract parameters, respectively. In addition, we propose adaptive parameter sampling to improve relative accuracy when the functionals have different magnitudes for different parameter sets. For calibration, we construct pricing surrogates for calibration instruments and optimize over them globally. We discuss strategies for robust calibration. We demonstrate the usefulness of our methodology on one-factor Cheyette models with benchmark rate volatility specification with an extra stochastic volatility factor on (two-curve) caplet prices at different strikes and maturities, first for parametric pricing, and then by calibrating to a given caplet volatility surface. To allow convenient and efficient simulation of processes and functionals and in particular the corresponding computation of samplewise derivatives, we propose to specify the processes and functionals in a low-code way close to mathematical notation which is then used to generate efficient computation of the functionals and derivatives in TensorFlow.

翻译:微分机器学习(Differential Machine Learning,DML)是一种近期提出的技术,它利用样本状态导数正则化最小二乘拟合,以学习随机过程泛函关于状态变量的条件期望。利用导数信息可在相同精度水平下,相比朴素机器学习方法减少所需样本数量。本文将该方法扩展至参数化问题,其中过程与泛函分别依赖于模型参数和合约参数。此外,我们提出自适应参数采样策略,以在泛函对不同参数集具有不同量级时提升相对精度。在校准方面,我们为校准工具构建定价替代模型,并在全局范围内对其优化。我们讨论了鲁棒校准策略。通过基于基准利率波动率规范的一因子Cheyette模型(额外包含随机波动率因子),对不同执行价和期限的双曲线上限期权价格进行参数化定价,并进一步校准至给定上限波动率曲面,我们验证了该方法的应用价值。为便捷高效地模拟过程与泛函,特别是计算对应的样本导数,我们提出以接近数学符号的低代码方式描述过程与泛函,并据此生成TensorFlow中泛函与导数的高效计算。