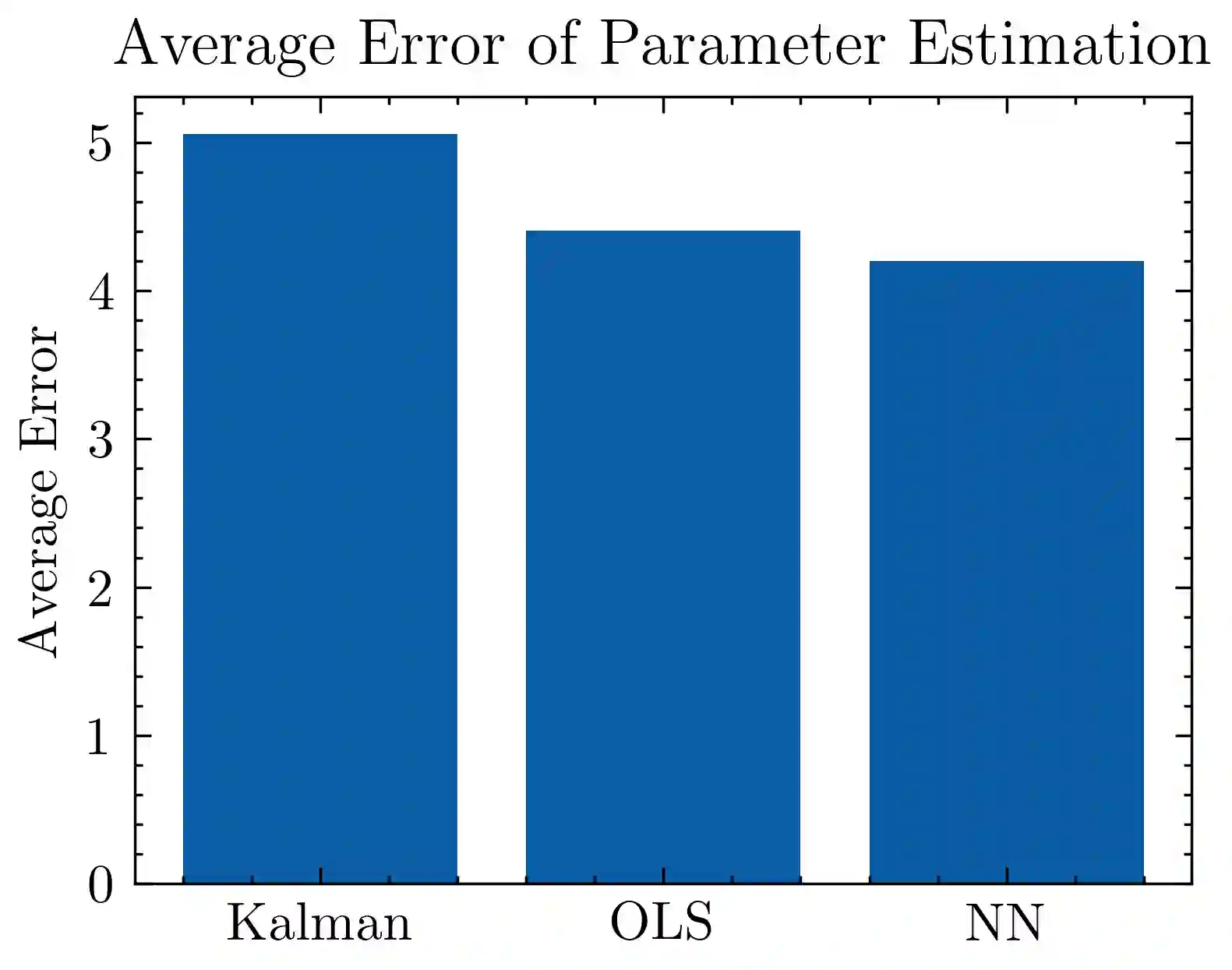

We consider the Ornstein-Uhlenbeck (OU) process, a stochastic process widely used in finance, physics, and biology. Parameter estimation of the OU process is a challenging problem. Thus, we review traditional tracking methods and compare them with novel applications of deep learning to estimate the parameters of the OU process. We use a multi-layer perceptron to estimate the parameters of the OU process and compare its performance with traditional parameter estimation methods, such as the Kalman filter and maximum likelihood estimation. We find that the multi-layer perceptron can accurately estimate the parameters of the OU process given a large dataset of observed trajectories and, on average, outperforms traditional parameter estimation methods.

翻译:我们考虑奥恩斯坦-乌伦贝克(OU)过程,一种广泛应用于金融、物理和生物学的随机过程。OU过程的参数估计是一个具有挑战性的问题。为此,我们回顾了传统跟踪方法,并将其与深度学习在估计OU过程参数中的新应用进行比较。我们使用多层感知器来估计OU过程的参数,并比较其与卡尔曼滤波和最大似然估计等传统参数估计方法的性能。研究发现,在拥有大量观测轨迹数据集的条件下,多层感知器能够准确估计OU过程的参数,并且平均而言优于传统参数估计方法。