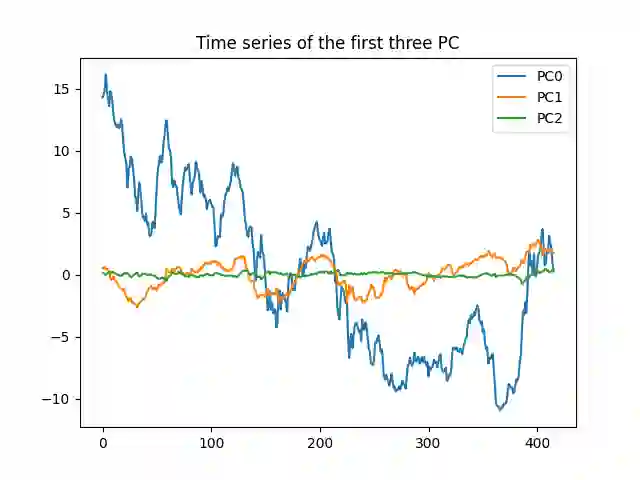

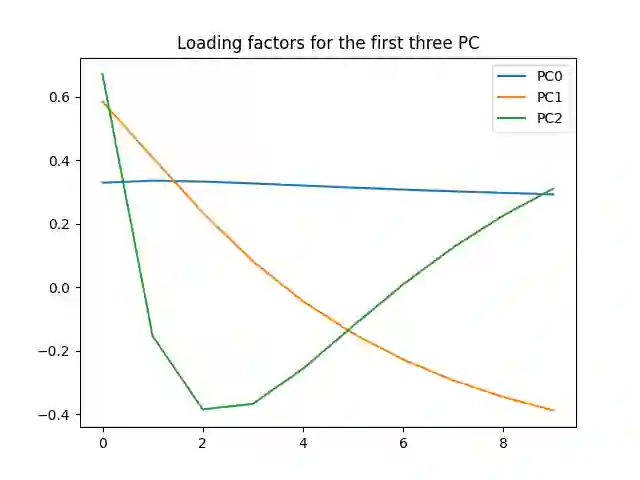

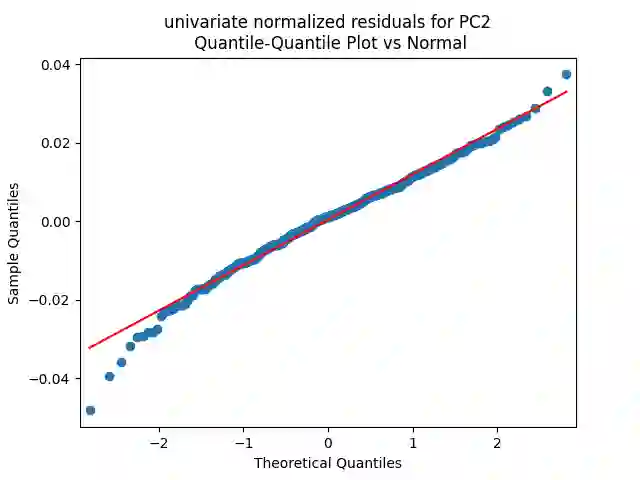

We study a multivariate autoregressive stochastic volatility model for the first 3 principal components (level, slope, curvature) of 10 series of zero-coupon Treasury bond rates with maturities from 1 to 10 years. We fit this model using monthly data from 1990. Next, we prove long-term stability for this discrete-time model and its continuous-time version. Unlike classic models with hidden stochastic volatility, here it is observed as VIX: the volatility index for the S\&P 500 stock market index. It is surprising that this volatility, created for the stock market, also works for Treasury bonds. Since total returns of zero-coupon bonds can be easily found from these principal components, we prove long-term stability for total returns in discrete time.

翻译:本文研究了一个多元自回归随机波动率模型,该模型针对10个期限(1至10年)的零息国债利率序列的前3个主成分(水平、斜率、曲率)构建。我们使用1990年以来的月度数据对该模型进行拟合。随后,我们证明了该离散时间模型及其连续时间版本具有长期稳定性。与经典的隐藏随机波动率模型不同,此处的波动率是可观测的,即VIX——标准普尔500股票市场指数的波动率指数。令人惊讶的是,这一为股票市场创建的波动率指标同样适用于国债。由于零息债券的总收益可以很容易地从这些主成分中推导得出,我们进一步证明了离散时间下总收益的长期稳定性。