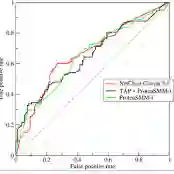

Standard risk models reduce the rich dependence structure of financial markets to scalar volatility estimates, discarding the topological information encoded in cross-asset correlation networks. We present ORCA (Online Regime Correlation Analyzer), an end-to-end framework that fuses spectral graph theory, random matrix theory, and supervised machine learning to deliver calibrated probability estimates for both rally and crash events over a ten-day forward horizon. ORCA constructs rolling correlation matrices from 24 diversified exchange-traded instruments using three parallel estimators at different time scales, and extracts 127 spectral features (absorption ratios, eigenvalue entropy, effective rank, spectral gap, eigenvector concentration, and graph-topological descriptors at multiple correlation thresholds), concatenated with 79 traditional price-derived indicators to form a 206-dimensional feature vector. A depth-limited Random Forest with balanced sub-sample weighting is evaluated under a strict eight-fold walk-forward protocol with ten-day anti-leakage gaps spanning fifteen years of daily US market data. ORCA achieves a Balanced Crisis Detection AUC (BCD-AUC, the geometric mean of rally and crash AUC) of 0.741, ranking first against all baselines. Ablation studies show that spectral features contribute +10.3 percentage points of AUC for crash detection and +5.2 for rally detection over traditional features alone, with SHAP analysis revealing that graph-topological descriptors (clustering coefficient, edge density, and dominant-eigenvalue percentile rank) are the three most important crash predictors. A backtested walk-forward strategy mapping the joint rally-crash signal to dynamic equity exposure with risk-on/risk-off rotation achieves a Sharpe ratio of 1.13, a CAGR of 15.6%, and a maximum drawdown of only -7.5%, versus 3.7% CAGR and -33.7% drawdown for buy-and-hold.

翻译:摘要:标准风险模型将金融市场丰富的依赖结构简化为标量波动率估计,从而丢弃了跨资产相关性网络中编码的拓扑信息。我们提出ORCA(在线市场状态相关性分析器),这是一个融合谱图论、随机矩阵理论与监督机器学习的端到端框架,能够针对未来十天的上涨与下跌事件提供校准后的概率估计。ORCA利用三种并行估计器在不同时间尺度上,从24种多样化交易所交易工具构建滚动相关性矩阵,并提取127个谱特征(包括吸收比、特征值熵、有效秩、谱隙、特征向量集中度以及多相关性阈值下的图拓扑描述符),同时结合79个传统价格衍生指标,形成206维特征向量。采用深度受限的随机森林与平衡子样本加权方法,在严格的八折滚动验证协议下进行评估,其间设置十天防泄漏间隔,涵盖十五年的美国市场日频数据。ORCA的平衡危机检测AUC(BCD-AUC,即上涨与下跌AUC的几何均值)达到0.741,在所有基线方法中排名第一。消融研究表明,相比仅使用传统特征,谱特征为下跌检测贡献了+10.3个百分点的AUC,为上涨检测贡献了+5.2个百分点。SHAP分析揭示,图拓扑描述符(聚类系数、边密度和主特征值百分位排名)是三个最重要的下跌预测因子。基于回测的滚动验证策略将联合上涨-下跌信号转化为动态权益敞口,并执行风险偏好/规避轮动,实现了1.13的夏普比率、15.6%的年化复合增长率,最大回撤仅为-7.5%;相比之下,买入并持有策略的年化复合增长率为3.7%,最大回撤为-33.7%。