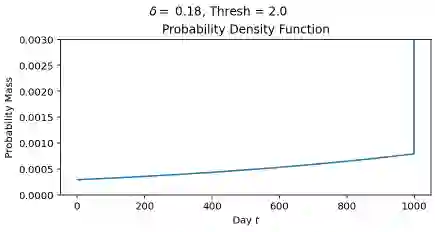

The classical ski-rental problem admits a textbook 2-competitive deterministic algorithm, and a simple randomized algorithm that is $\frac{e}{e-1}$-competitive in expectation. The randomized algorithm, while optimal in expectation, has a large variance in its performance: it has more than a 37% chance of competitive ratio exceeding 2, and a $\Theta(1/n)$ chance of the competitive ratio exceeding $n$! We ask what happens to the optimal solution if we insist that the tail risk, i.e., the chance of the competitive ratio exceeding a specific value, is bounded by some constant $\delta$. We find that this additional modification significantly changes the structure of the optimal solution. The probability of purchasing skis on a given day becomes non-monotone, discontinuous, and arbitrarily large (for sufficiently small tail risk $\delta$ and large purchase cost $n$).

翻译:经典滑雪租赁问题有一个教科书式的2-竞争比确定性算法,以及一个简单的随机化算法,其期望竞争比为$\frac{e}{e-1}$。该随机化算法虽然在期望意义下最优,但其性能方差较大:竞争比超过2的概率超过37%,且竞争比超过$n$的概率为$\Theta(1/n)$!我们探究:若强制要求尾部风险(即竞争比超过特定值的概率)被某个常数$\delta$所界定时,最优解会发生什么变化。我们发现,这一额外修正显著改变了最优解的结构。在给定天购买滑雪板的概率变得非单调、非连续,且可能任意大(当尾部风险$\delta$足够小且购买成本$n$足够大时)。